- Debt settlement and debt consolidation solve different problems — settlement negotiates your balance down; consolidation restructures your debt into a single, lower-rate payment — and choosing the wrong one can cost you years of credit recovery.

- The dividing line between them is usually your credit score and how far behind you are — readers still current on payments and above a 580 score almost always qualify for consolidation; settlement is a last resort for those already seriously delinquent.

- The cost gap between the two options is wider than most people realize — settlement fees typically run 15–25% of enrolled debt plus potential tax liability on forgiven amounts, while consolidation's main cost is the loan's interest rate.

Short answer: if you still qualify for a loan, consolidation wins. Settlement is for accounts already in collections with no realistic path to new credit.

You’ve been watching the same credit card balances barely move for months, and now you’re seeing ads for debt settlement companies promising to cut what you owe in half. It sounds appealing. But is it actually better than a consolidation loan?

Debt consolidation vs. settlement is one of the most misunderstood choices in personal finance. Both options claim to help you escape debt, but they work in completely opposite ways. Choosing the wrong one can lock you into years of credit damage or a fee structure that costs more than the debt you were trying to escape.

This article gives you a straight answer on which path fits your situation — not a pitch for either industry. We start with a quick decision tool, then explain how each option works, what it actually costs, and when one clearly beats the other.

Quick Answer

Credit score above 580, accounts not in collections: Consolidation is the stronger option — lower fees, preserved credit, and a predictable payoff date.

90+ days delinquent, score below 580, already denied for a loan: Settlement may be your most realistic path — but enter it with clear eyes on the fees, the tax bill, and the 7-year credit mark.

Which Option Fits Your Situation?

Before diving into the mechanics, run through these three questions. They’ll route you to the right section.

Question 1: Is your debt already severely delinquent — 90+ days past due, or in collections?

- Yes → Move to Question 2.

- No → Consolidation is likely available to you. Skip to the What Debt Consolidation Actually Is section below.

Question 2: Has your credit score already fallen below 580, or has any account been charged off (written off as a loss by your lender, typically after 180 days without payment)?

- Yes → Move to Question 3.

- No → Consolidation is still the stronger option. Your credit can recover faster. Skip to the consolidation section.

Question 3: Have you already been denied for a personal loan or balance transfer?

- Yes → Debt settlement may be your most realistic path. Read the settlement section first — the fees and credit consequences are significant.

- No → Try consolidation first. You may still qualify.

If you’re unsure, read both sections — the comparison table further down shows exactly what each option costs across the factors that matter most.

What Is Debt Settlement and How Does It Work?

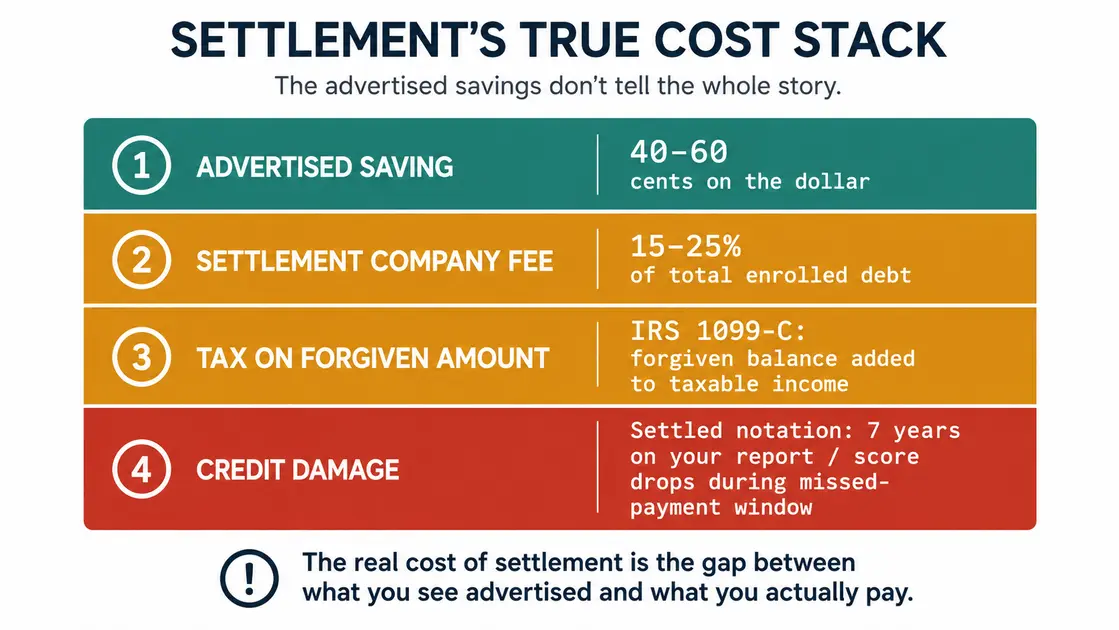

Debt settlement is a negotiation process. You — or a company acting on your behalf — contacts your creditors and offers to pay a lump sum that is less than the full amount you owe. Creditors typically accept somewhere between 40 and 60 cents on the dollar.

That sounds like a good deal. The catch is in how you get there.

How the process actually works

Creditors will only settle when they believe partial payment is better than nothing. That belief only kicks in when they’re convinced you genuinely cannot pay the full amount. In practice, this means accounts usually need to be 90 or more days delinquent before a creditor is willing to negotiate at all.

This is not an incidental side effect of the settlement process. For most settlement programs, letting your accounts go delinquent is a deliberate part of the strategy. You stop making payments, accumulate the missed-payment damage on your credit report, and use that period to build up a lump sum in a separate account that you’ll eventually use to negotiate.

Who handles the negotiation

You have two options. You can negotiate directly — call the creditor’s hardship or settlement department, explain that the account is past due, and offer a one-time settlement. This works best when you have a lump sum ready and the account is already delinquent. Get any agreement in writing before you pay anything.

The alternative is hiring a debt settlement company. They handle the calls and negotiations for a fee — typically 15–25% of the total enrolled debt. If you’re carrying $20,000 in debt and they settle for $12,000, their fee is calculated on $20,000, not $12,000. Doing it yourself and avoiding that fee is worth considering seriously. Note that under the FTC’s Telemarketing Sales Rule, settlement companies are legally prohibited from collecting any fees before they’ve successfully settled at least one of your accounts — if a company demands upfront payment, walk away.

What settlement actually costs — the full picture

The headline of “40 cents on the dollar” leaves out three costs that change the math considerably.

First, company fees: 15–25% of enrolled debt.

Second, debt settlement tax consequences. The IRS treats forgiven debt as taxable income. If a creditor forgives $5,000, they file a 1099-C (a tax form reporting the forgiven amount as income you received). That $5,000 is added to your taxable income for the year — a real bill that arrives the following April. Important exception: under IRC Section 108, if you are insolvent at the time of cancellation — meaning your total debts exceed your total assets — you can exclude the forgiven amount from taxable income up to the extent of that insolvency. Most people who qualify for debt settlement are insolvent by this definition. Complete IRS Form 982 and see IRS Publication 4681 for details, or consult a tax professional before assuming you’ll owe the full tax on a forgiven balance.

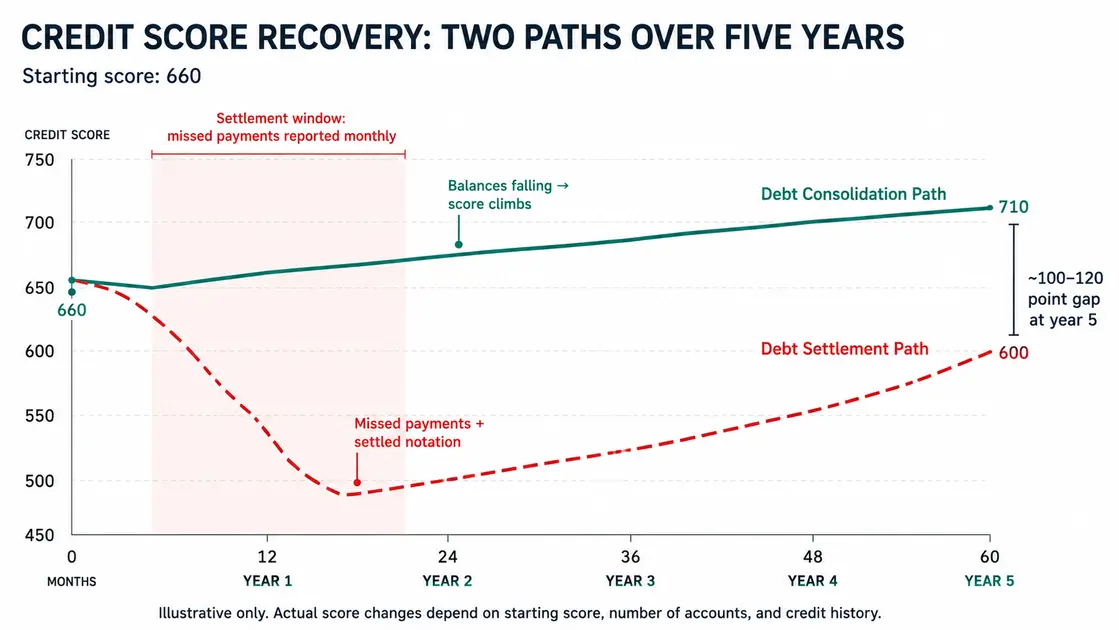

Third, credit damage. A settled account is reported as “Settled” rather than “Paid in Full.” To future lenders, those phrases mean very different things. A settled account stays on your credit report for 7 years from the date of original delinquency. And during the settlement window — the months you’re missing payments to build a lump sum — every missed payment is reported and your score drops continuously.

Who settlement realistically makes sense for

Settlement is appropriate when you are already severely delinquent (90+ days behind or charged off), cannot qualify for new credit, are facing creditor lawsuits or wage garnishment threats, and have access to a lump sum — whether from savings, family, or an asset sale — to offer creditors. If you’ve already had a personal loan application rejected because of your credit situation, settlement may be the most practical path available to you. If you’re already in this position, settlement is still a way out — it’s just one to enter with clear eyes on the full cost and timeline.

What Is Debt Consolidation and How Is It Different From Settlement?

Debt consolidation takes a fundamentally different approach. Instead of reducing what you owe, it restructures how you pay it. You take out a new loan — typically a personal loan — at a lower interest rate and use it to pay off multiple existing debts. The result: one monthly payment, one interest rate, and a defined end date.

How it works

Most consolidation is done through a personal loan for debt consolidation. You borrow a fixed amount, receive the funds, pay off your credit cards or other unsecured debts, and then repay the personal loan over 2–5 years at a fixed rate. A less common alternative is a balance transfer credit card, which moves credit card balances onto a single card at a 0% introductory APR for 12–21 months — a solid option if you can pay the balance off within the promotional window. For readers carrying multiple types of unsecured debt, the personal loan route is usually more practical.

What it actually costs

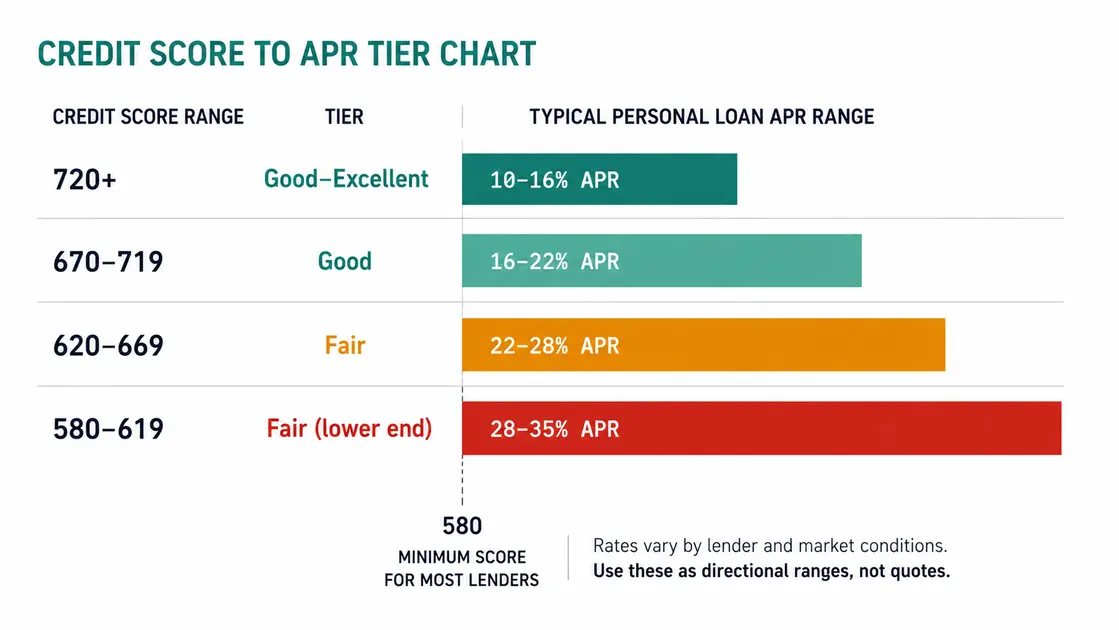

The interest rate is the primary cost — and it depends almost entirely on your credit score. A 720 score might unlock roughly 10–16% APR from most lenders, with select credit unions going lower; a 580 score typically faces 24–35% APR. Exact rates shift with market conditions, so treat these as directional ranges rather than quotes.

This is worth understanding before you apply, because how your credit score affects what a lender charges you determines whether the consolidation loan actually saves you money versus your current situation.

Most lenders also charge origination fees (an upfront cost, typically 1–8% of the loan amount, either deducted from what you receive or rolled into the balance). If the consolidated rate isn’t meaningfully lower than your current weighted average interest rate (the blended rate across all your debts, weighted by balance), the benefit shrinks significantly — run the math before signing.

What changes for the reader

One fixed monthly payment replaces your current mix of variable minimums. A hard inquiry will hit your credit report when you apply — typically a 5-point drop that recovers within 12 months. Importantly, consolidation does not eliminate debt. The total balance is the same; the terms change. For readers weighing a balance transfer instead, the debt consolidation vs. balance transfer comparison is worth reading separately.

Who consolidation makes sense for

This option works when you’re still current on payments or only 30–60 days behind, have a credit score of 580 or higher, carry multiple high-rate unsecured debts, and have stable income to support fixed monthly payments. Debt consolidation with bad credit is possible at the lower end of that score range — but the rate will be significantly higher, and you need to verify it still beats your current rates before proceeding.

A third option worth knowing: If you’re current on payments but can’t qualify for a personal loan, a nonprofit debt management plan (DMP) through an NFCC-member credit counseling agency is worth looking into. It’s not consolidation and not settlement — the agency negotiates reduced interest rates with your creditors and you make one monthly payment to them. Fees are substantially lower than for-profit settlement companies, and it doesn’t require you to go delinquent.

What Are the Key Differences Between Debt Settlement and Debt Consolidation?

Here’s how the two options compare across the factors that actually matter when you’re choosing between them.

| Category | Debt Settlement | Debt Consolidation |

|---|---|---|

| How it works | Negotiates a reduced balance with creditors | Combines debts into one new loan at a lower rate |

| Credit score impact | Severe — settled accounts remain 7 years; score can drop 100+ points | Moderate — hard inquiry + possible score improvement as balances fall |

| Total cost | Reduced balance minus fees (15–25%) + potential tax on forgiven amount | Full balance repaid + interest + origination fee |

| Timeline | 2–4 years (while building lump sum) | 2–5 years (fixed loan term) |

| Who qualifies | Severely delinquent, unable to get new credit | Credit score 580+, stable income |

| Risk level | High — collections and lawsuits possible during process | Low-to-moderate — mainly interest rate risk |

| Effect on collections | Does not stop collection activity during process | Pays off debts immediately; collections stop |

The table makes it look like a close call. It isn’t — for most readers who still qualify for a consolidation loan, the credit and cost math heavily favors consolidation.

Which Option Actually Wins for Your Financial Situation?

For most borrowers who are still current on payments and have a credit score above 580, debt consolidation is the better option. Debt settlement is a last resort for accounts that are already charged off with no realistic path to qualifying for new credit.

Here’s why the math supports it.

Debt consolidation costs you the full balance plus interest — but avoids every piece of collateral damage that comes with settlement. No 7-year credit mark from a “Settled” notation. No surprise tax bill on forgiven amounts. No settlement company fees. No months of missed payments dragging your score lower while you build a lump sum. No creditor lawsuits landing while you’re mid-process. The total cost of a consolidation loan is predictable from day one. The total cost of settlement is not.

Debt settlement is the right call in a narrow set of circumstances: accounts already charged off, score already below 580 from existing delinquency, no realistic path to qualifying for a personal loan. For readers in that position, settlement can be the most practical exit from a situation that is already past the point where credit preservation matters.

The most useful single heuristic: if your score is still above 580 and your accounts haven’t been charged off, try consolidation first. Even a higher-rate consolidation loan in the 24–35% APR range is likely a better outcome than the settlement process — because consolidation keeps your credit functional for future borrowing. The difference between “settled” and “paid in full” on a credit report is not cosmetic. After settlement, you’re looking at 3–5 years of rebuilding before major lenders take you seriously again.

If consolidation is the right path, the next question is whether you qualify and what the actual monthly payment looks like. You can also read more about how to consolidate credit card debt with a personal loan to understand what the application process involves.

How Much Could Debt Consolidation Actually Save You?

Consolidation Savings Estimator

Loan vs. Minimum Payments — Side by Side

Enter your total debt, the consolidation loan rate you expect to receive, and your preferred repayment term. The calculator shows your fixed monthly payment and total interest under a personal loan — compared with what staying on minimum payments would actually cost you.

Check If You Qualify for a Personal Loan

Checking available rates won't affect your credit score.

Check If You Qualify for a Personal Loan →We earn a commission if you apply through links on this page. This doesn’t change our analysis — both options are covered on their merits.

Bottom line: If your score is above 580 and your accounts are current, consolidation is the cleaner exit — predictable cost, no tax liability, and no 7-year settled mark. Checking your rate takes under 2 minutes and won’t affect your credit score.

Frequently Asked Questions

Will debt settlement ruin my credit score?

Settlement causes significant credit damage — but "ruin" depends on your starting point. Accounts typically need to be 90+ days delinquent before creditors will negotiate, and those missed payments are already damaging your score before settlement even begins. Once settled, the account is marked "Settled" rather than "Paid in Full" and stays on your credit report for 7 years. The cumulative drop — from the months of missed payments during the settlement window plus the final settled notation — typically runs 75–150 points from your pre-delinquency score. Most of that damage comes from the missed payments, not the settlement itself. Recovery takes 3–5 years of consistent positive behavior.

Is debt settlement the same as debt consolidation?

No — they solve debt problems in opposite ways. Settlement negotiates your total balance down so creditors accept less than you owe. Consolidation pays your balances in full by replacing them with a single new loan at a lower interest rate. Settlement damages your credit significantly; consolidation typically has only a minor short-term impact. The only thing they share is that both aim to simplify or resolve debt — but the mechanism, cost structure, and credit outcome are entirely different.

How long does debt settlement stay on your credit report?

A settled account stays on your credit report for 7 years from the date of original delinquency — not the settlement date. After 7 years it falls off automatically. Its negative weight does decrease over time: a settled account from 5 years ago affects your score far less than one from 6 months ago. Note that the tax liability from forgiven debt — reported via IRS Form 1099-C — is a separate matter that surfaces in the tax year the debt is forgiven, regardless of how many years later that is.

Do I need a debt settlement company or can I negotiate myself?

You can negotiate directly, and it often works better than using a company — especially if you have a lump sum ready and the account is already delinquent. Call the creditor's hardship or settlement department, state that you can offer a one-time settlement payment, and get any agreement in writing before paying. Settlement companies charge 15–25% of enrolled debt — DIY negotiation avoids that fee entirely. The main reason to use a company is if you have multiple accounts and don't want to manage the process across several creditors simultaneously.

What credit score do I need to qualify for a consolidation loan?

Most personal loan lenders require a minimum score of 580–620, though rates at that range — typically 24–35% APR — are high enough that the loan needs to replace significantly higher-rate debt to make sense. A score of 670 or above unlocks meaningfully better terms. If you've been denied, check credit unions, community banks, or secured loan options — they often apply more flexible criteria than online lenders. Understanding why minimum payments keep you in debt can help you decide whether to apply now or spend a few months improving your score first. If the constraint goes beyond the score — income stretched with no margin — getting out of debt when you're broke covers the steps that create room before consolidation becomes feasible.

Can I consolidate debt that's already in collections?

In most cases, no — traditional personal loan lenders will not extend credit to applicants with active collection accounts. Collections signal to lenders that prior obligations were not repaid, which makes you a high default risk. Some lenders specializing in bad-credit personal loans may approve applications with older or smaller collection accounts, but rates will be high. If your debt is already in collections, settlement or a debt management plan through a nonprofit credit counseling agency is likely more realistic than a standard consolidation loan.

Is debt consolidation the same as bankruptcy?

No — they're fundamentally different and produce very different outcomes. Debt consolidation is a loan: you repay everything you owe, just under better terms. Bankruptcy is a legal process that either eliminates debt (Chapter 7) or restructures it under court supervision (Chapter 13). Bankruptcy has the most severe credit impact of any option — it stays on your report for 7–10 years depending on type — but provides legal protection from collections and lawsuits that neither consolidation nor settlement can offer. Bankruptcy is a last resort when debt is simply unpayable in any restructured form.

If your accounts are still current and your credit score is above 580, a personal loan is likely the cleaner path — without the settlement fees, tax liability, or 7-year credit mark.