- Why minimum payments are structured to keep accounts current — not eliminate debt — and how daily interest accrual quietly consumes most of what you pay each cycle.

- Who gets trapped longest — borrowers who pay on time every month but never see why the balance barely moves despite consistent payments and no missed cycles.

- What the math actually shows about minimum-only versus fixed payments — and what a $75-per-month increase does to a 20+ year repayment timeline on a $5,000 balance.

You look at the balance. It’s almost exactly what it was three months ago.

You haven’t missed a payment. You’ve sent money every single cycle. The account is current, the card is in good standing — and the balance is barely moving. At some point you stop expecting it to drop and start wondering whether it actually can.

That’s not paranoia. That’s the predictable result of how minimum payments are built.

Minimum payments are not designed to eliminate debt. They’re designed to keep your account current. That’s the entire purpose — and once you understand the mechanics behind it, the stagnant balance makes complete sense.

Many cards now carry APRs above 20%, according to Federal Reserve data. The Federal Reserve has tracked total revolving credit card debt past $1 trillion. Most cardholders pay only the minimum — or close to it — each month. What feels like responsible repayment quietly becomes a years-long obligation.

Why So Many People Feel Stuck in Credit Card Debt

The frustration isn’t a discipline problem. You’re not ignoring the bill. You’re doing exactly what the statement asks — and the debt won’t move. The danger isn’t missing payments. It’s staying in debt for years while faithfully making them. To understand why, you need to see the mechanics behind the number on your statement.

What Is a Minimum Payment and Why Doesn’t It Eliminate Debt?

A minimum payment is the smallest amount required to keep your account in good standing. It prevents late fees and delinquency reporting. What it does not do is make a meaningful dent in your actual debt.

Issuers calculate minimums a few ways:

- A flat dollar amount (typically $25–$35)

- A percentage of your balance, usually 1–3%

- The greater of the two above

- Interest charges plus fees, plus a small slice of principal

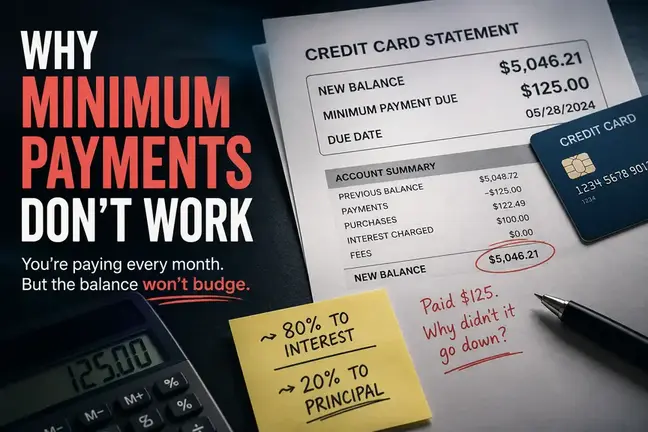

On a $5,000 balance at 24% APR, that often lands around $100–$125. That number looks manageable. The problem is what happens inside that payment.

How Credit Card Companies Calculate Minimum Payments

Most issuers use a percentage-based formula that shrinks your minimum as your balance falls. Owe $5,000, pay $125. Pay it down to $4,500, your minimum drops to $112. Then $101. Lower still.

Falling minimums can feel like progress. They’re not. The less you owe in theory, the less principal you’re required to attack — and the timeline stretches further. Payments are also applied to interest first. Whatever remains goes toward principal. That sequencing is where most cardholders lose ground.

Why Minimum Payments Exist in the First Place

Minimums weren’t designed with your payoff speed in mind. They exist to reduce default risk for the lender. As long as you’re paying something, the account stays open, the balance keeps generating interest, and the issuer avoids a charge-off. The CFPB is clear that minimum payment structures are designed to keep accounts current — not to optimize repayment for the borrower.

Why Does Your Balance Barely Go Down Even When You Pay Every Month?

Credit card interest doesn’t accumulate once a month. It compounds daily, based on your average daily balance. By the time your payment posts, a significant portion is already absorbed by interest charges that built up since your last cycle.

Where Most of Your Payment Actually Goes

At 24% APR, a $5,000 balance generates roughly $100 in interest every single month — before your payment even arrives.

Here’s what that means in practice:

- Balance: $5,000

- APR: 24% (monthly rate: 2%)

- Interest charge: $5,000 × 2% = $100

- Minimum payment: $125

- Applied to principal: $25

80% of your payment disappeared before touching the actual debt. You paid $125 and reduced your balance by $25. If you made any new purchases that month, the principal may not have moved at all.

The payment felt productive. The math says otherwise.

The Difference Between Interest and Principal

Principal is the actual amount you borrowed — the real debt. Every dollar that reduces it is real progress.

Interest is the cost of borrowing. It’s charged on your outstanding balance every month and does nothing to reduce what you owe. It’s the price of carrying the debt.

When most of your minimum goes to interest, principal barely shrinks. And because interest is recalculated on the remaining balance each cycle, next month’s charge is nearly identical to this month’s. The meter keeps running at almost the same rate.

Why High APR Debt Feels Impossible to Escape

At 24% APR, the math is already brutal. At 29% — which many cards now carry — it’s worse. The higher the rate, the more every payment is consumed by interest before a dollar reaches principal. Keeping a high balance also elevates your credit utilization, which creates downstream consequences for your credit profile — a cycle that compounds the problem beyond just the debt itself.

The minimum payment creates the illusion of control because the account remains current. Nothing feels broken. The financial damage happens slowly enough to normalize.

How Long Can Minimum Payments Keep You in Debt?

A Small Monthly Payment Can Add Years to Repayment

What felt manageable at checkout can become a decade-long repayment cycle. Here’s what the numbers actually show on a $5,000 balance at 22% APR:

| Minimum Payments Only | Fixed $200/Month | |

|---|---|---|

| Monthly payment | ~2% of balance (shrinks over time) | $200 fixed |

| Time to pay off | 20+ years | ~3 years |

| Total interest paid | $8,000–$15,000+ | ~$1,700 |

| What’s happening | Each payment is mostly interest; minimum shrinks as balance drops, slowing progress further | Extra dollars hit principal directly; less principal = less interest next cycle; payoff accelerates |

The same $5,000. The same person. The only difference is $75 more per month — and 17+ fewer years.

Use the credit card minimum payment calculator to run the same comparison against your own balance, APR, and payment amount.

A temporary balance quietly becomes a long-term obligation — not because the borrower stopped paying, but because the repayment structure was never designed for speed. Once you’re ready to move beyond minimums, the next question is which debt to attack first — the debt snowball vs. avalanche comparison walks through exactly how to structure a concentrated payoff plan.

Why Debt Payoff Slows Down Over Time

As your minimum shrinks alongside your balance, so does the principal attack. Progress that already felt slow becomes imperceptibly slower. The CFPB requires credit card statements to include a “Minimum Payment Warning” showing the estimated payoff timeline and total interest under minimum-only payments. That number is typically alarming. Most people never read it.

What Is the Minimum Payment Trap Most People Don’t Realize They’re In?

The problem doesn’t stay contained to your credit card. It moves through your broader financial life through a cycle that’s easy to miss until you’re deep in it:

High balance → High interest → Small principal reduction → Elevated utilization → Lower credit score → Higher borrowing costs → Debt persists

How Carrying Balances Affects Your Credit Score

Credit utilization — the percentage of available revolving credit currently in use — is one of the most heavily weighted factors in FICO scoring. Carrying balances at 50%, 70%, or 90% of your limit signals financial stress to lenders and can meaningfully drag down your credit score and loan rates — even without a single missed payment.

Why Long-Term Debt Gets More Expensive

A lower score changes the terms you’re offered on every future loan — auto, personal, mortgage. Understanding how your credit score affects your loan interest rate makes the connection concrete: revolving debt today increases your borrowing costs tomorrow. The credit card problem becomes a full borrowing cost problem. Once balances come down, building credit without carrying revolving debt is the logical next step — one that doesn’t require going back into debt to improve your profile.

Why Do Credit Card Companies Structure Minimum Payments This Way?

Issuers are in the business of lending money and collecting interest. Minimum payments keep accounts current — borrowers don’t default, issuers don’t write off bad debt. It’s risk management on their side of the table.

Revolving Debt Is Extremely Profitable

A cardholder who carries a $5,000 balance for five years generates significantly more revenue for an issuer than one who pays it off in six months. The Federal Reserve’s consumer credit data consistently shows that revolving balances represent a substantial share of credit card industry revenue. Long-term balances produce predictable, recurring interest income.

The System Rewards Long Repayment Timelines

Extended repayment means extended interest collection. The structure of minimum payments — shrinking amounts, interest-first allocation — naturally produces that outcome. The CFPB studied this and required clearer disclosures as a result. Knowing the structure doesn’t change the math on its own. Changing the payment does.

How Do You Know If You’re Already Stuck in the Minimum Payment Cycle?

Here’s the one that tends to land first: the interest charge on your last statement was more than half your payment. That’s the number that makes the problem visible.

Other signals that the cycle is already running:

- Balance barely changes month to month despite consistent payments

- Credit utilization stays above 30% month after month

- The debt has been on the card for over a year with no meaningful reduction

- You’re using one card for expenses while carrying a revolving balance on another

- The balance has started to feel permanent rather than temporary

Why This Cycle Often Feels Invisible at First

In the beginning, minimum payments feel responsible. The account is current. Nothing is overdue. The repayment structure gives you no urgent signal that something is wrong.

But the debt mechanics are working quietly. Interest accumulates daily. Principal shrinks by almost nothing. By the time the timeline becomes visible — by the time someone actually reads the minimum payment warning — years of compounded interest may have already passed.

What Actually Starts Reducing Credit Card Debt Faster Than Minimum Payments?

Why Paying Slightly More Changes the Repayment Math

When you pay above the minimum, the surplus goes almost entirely to principal. Less principal means less interest next month. Less interest means more of your next payment reaches principal. The interest suppression compounds — faster than most people expect.

Going from $125 to $200 per month on a $5,000 balance doesn’t just accelerate payoff. It fundamentally changes the interest structure of every subsequent payment.

That’s why the two scenarios above diverge so sharply. The extra $75 triggers a positive repayment cycle rather than a stagnant one.

This same math shapes the decision between paying off debt and investing. When APR is high, guaranteed interest elimination often outperforms uncertain investment returns.

Lower APR Compresses the Timeline Directly

Reducing the rate changes the math at the source. At 24% APR, $100 of every monthly payment on a $5,000 balance is consumed by interest. At 14% APR, that drops to roughly $58.

The same payment does dramatically more work — more principal reduction, faster payoff, lower total cost.

Options for rate reduction include balance transfer cards with promotional 0% periods, personal loan consolidation at a fixed lower rate, or direct negotiation with your issuer. Between the first two, the answer isn’t obvious — Debt Consolidation vs Balance Transfer runs the numbers on both and shows where each option wins. For the full picture on whether a personal loan consolidation saves money in your case — including what origination fees do to the math and how to avoid the reloading trap — see the complete guide here. Eligibility depends on your credit profile. If past debt has already created friction with lenders, understanding why loan applications get rejected is worth knowing before applying.

What Is the Real Total Cost of Only Paying the Minimum Each Month?

The Financial Costs

The direct cost is interest — thousands of dollars paid over years for debt that the repayment structure was quietly designed to extend.

The secondary cost is opportunity cost. Every dollar absorbed by interest is a dollar that isn’t building savings, funding retirement, or creating financial flexibility. High utilization also constrains borrowing options at exactly the moments they’re needed most — emergencies, large purchases, refinancing opportunities.

That last point compounds quietly: minimum payments leave no room to build a financial buffer. When the next unexpected expense hits — a car repair, a medical bill — there’s nowhere to absorb it except the credit card. Every emergency reloads the balance you’ve been paying down. Building even a $500 starter emergency fund while servicing debt is what breaks that cycle.

Minimum payments also create a structural problem for percentage-based budgets: they sit in the needs bucket by definition, and at high APRs they can absorb 8–10% of take-home pay before a single lifestyle expense is counted. The 50/30/20 rule’s 50% needs ceiling breaks for exactly this reason. If you haven’t yet mapped these numbers against your take-home, building a monthly budget from scratch is where the minimum payment line’s true weight — relative to income and every other committed cost — becomes concrete.

The Weight of Going Nowhere

Paying consistently while going nowhere creates a specific kind of exhaustion. It’s not the exhaustion of missing payments or falling behind — it’s quieter than that. It’s the exhaustion of doing everything right and watching the number barely move.

Eventually that exhaustion leads to disengagement — the point where people stop checking, stop calculating, and just send the payment. Which is exactly when the debt mechanics run most efficiently.

That’s the real cost. Not just the thousands in interest. The years of financial energy spent on a number that doesn’t move.

If the financial pressure extends beyond the card itself — if managing all of this alongside everything else has become genuinely overwhelming — Financial Help Finder searches available assistance programs matched to your situation. Free to check, no purchase required.

Why Does Understanding the Minimum Payment System Matter for Getting Out of Debt?

Minimum payments prevent default. That matters — missing a payment carries real consequences in fees, credit damage, and potential rate increases. If you’ve already missed one, this covers the exact timeline from day 1 to day 30 — and what to do right now. If the balance has become overwhelming enough that stopping payments entirely has crossed your mind, the full sequence from first missed payment to charge-off — and the hardship exits available at each stage before it becomes irreversible — is covered here.

But a minimum payment is a floor, not a strategy.

Daily interest accrual, interest-first payment allocation, and shrinking minimums create a repayment structure that can stretch debt over decades and cost far more than the original balance. Most people don’t lose to debt because they stop paying. They lose because they never see how slowly the balance is actually moving.

One Thing You Can Do With This

Check your last statement. Look at the interest charge line. If it’s more than half your payment, the cycle described above is already running on your account — and the minimum payment warning at the bottom of your statement will show you what that math produces over time.

The floor-versus-strategy distinction is the thing to hold onto. Paying the minimum keeps the account in good standing. Paying above it — even $50 more — starts suppressing future interest. Those aren’t the same thing.

For the next layer, the relationship between credit utilization and your broader financial profile shows how the credit card problem connects to borrowing costs on everything else. If the goal is also to rebuild your score after clearing the debt, you can build a strong credit profile without carrying revolving balances.

Where to Start Based on Where You Are

Your balance is under $5,000 → A balance transfer to a 0% APR card is likely your fastest, cheapest path. The transfer fee (3–5%) is usually less than 2–3 months of current interest charges. Compare balance transfer vs. consolidation loan options to see which saves more on your specific balance.

Your balance is $5,000–$15,000 → Two paths: either increase your monthly payment to at least double the minimum, or consolidate into a personal loan at a lower APR. The consolidation option matters most if your card APR is above 20%. See if the APR math makes consolidation worth it.

Multiple cards at minimum payments → Pick which debt to attack first with a structured payoff method. The debt snowball vs. avalanche comparison shows which method saves more money and which one you’re more likely to finish.

Frequently Asked Questions About Minimum Payments

Why is my credit card balance not going down even though I pay every month?

Because most of your minimum payment is being consumed by interest before it reaches your principal. At a typical APR of 20–24%, a $5,000 balance generates $83–$100 in interest per month. If your minimum is $125, only $25–$42 is actually reducing your debt. The rest disappears into interest. The balance looks the same because the debt math is working exactly as designed.

How long will it take to pay off $5,000 in credit card debt on minimum payments?

At 20–24% APR on minimums only, roughly 15 to 20 years — and you'll pay $4,000 to $6,000 in interest on top of the original $5,000. Your card statement is legally required to show this estimate in the minimum payment warning box. Most people scroll past it without reading it.

What happens if I only pay the minimum on my credit card every month?

Your account stays current (no late fees, no credit damage from missed payments), but your balance barely moves. Each month, the majority of your payment covers interest. The minimum itself shrinks as your balance drops — which sounds like progress but actually means even less principal gets paid each cycle, stretching the payoff timeline further.

How much should I pay on my credit card to actually make progress?

At minimum, pay enough to cover the full interest charge plus a meaningful slice of principal. In practice, that means paying at least 2× the minimum — but 3× or more is where you start seeing real monthly progress. On a $5,000 balance at 22% APR, bumping from $125 to $200 per month cuts payoff from 17+ years to about 3 years and saves roughly $4,000 in interest.

Does paying only the minimum hurt my credit score?

Not directly — paying the minimum on time keeps your payment history clean. But it does hurt your score indirectly by keeping your credit utilization high. A $5,000 balance that barely moves each month keeps your utilization elevated, which suppresses your FICO score and increases the rate you'll be offered the next time you need to borrow.

Can I negotiate a lower interest rate with my credit card issuer?

Yes, and it costs nothing to ask. Call the number on the back of your card, reference your payment history (especially if it's clean), and ask for a rate reduction. Issuers often prefer a modest rate adjustment over losing the account to a balance transfer. It doesn't always work, but it works often enough to be worth a 10-minute phone call — and even a 3–5 point reduction meaningfully changes the payoff math.

What's the difference between the minimum payment and what I should actually pay?

The minimum keeps your account in good standing. What you should actually pay is whatever amount results in meaningful principal reduction each month — typically the full balance if you can manage it, or at minimum a fixed amount well above the minimum. The simplest guideline: if the interest charge on your statement is more than half your payment, your current payment isn't working.

What if I can't afford to pay more than the minimum right now?

Start by calling your issuer to request a hardship plan or rate reduction — issuers have programs that aren't advertised. The other move is looking at whether restructuring makes sense: a balance transfer to a 0% card or a consolidation loan at a lower APR can make the same payment go much further against the actual debt. Even a 5-point APR reduction changes the timeline significantly. If the constraint is structural — income fully committed with nothing left over — the six-step approach for getting out of debt when you're broke covers the path forward.

Financial Assistance

Sometimes the Math Isn't the Only Problem

If managing this balance alongside other financial pressures has become overwhelming, Financial Help Finder searches available grant and assistance programs matched to your situation — free to use, no purchase required.

See What's Available →Financial Decision Lab provides educational content about personal finance topics. This article is for informational purposes only and does not constitute financial or legal advice. Readers should consult with a qualified financial professional before making financial decisions.