- Why your credit score — not your income — is the single biggest variable in what a lender charges you, and how to see the exact dollar gap between tiers.

- Who gets hit hardest by the rate gap — and why most borrowers don’t realize it until after they’ve already signed.

- What moves a score between tiers, how long it realistically takes, and what one tier shift saves on a real loan.

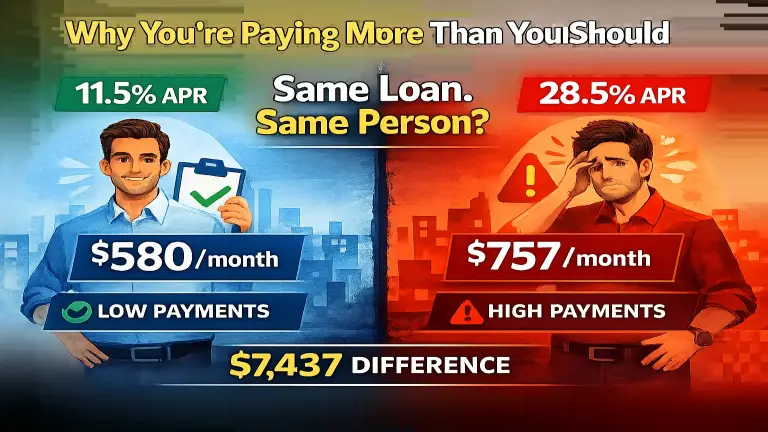

Andy and Tim are both 31 years old. They work in the same city, earn similar salaries, and on the same afternoon they each apply for a $20,000 personal loan over 42 months.

Same loan. Same day. Same lender.

Andy walks away with an 11.5% APR. Tim gets 28.5%.

That’s not a clerical error. It’s not arbitrary. It’s the direct result of what their credit profiles communicated to the lender before either of them said a word.

Here’s what that difference actually costs:

- Andy pays $580.68/month — total interest paid over 42 months: $4,388

- Tim pays $757.73/month — total interest paid over 42 months: $11,825

Tim pays $7,437 more in interest. On the exact same loan amount. Over the exact same period.

What would that gap look like on your loan? Run the numbers:

Loan Cost Calculator

⚠ Estimates only. APR figures are averages based on recent market data — your actual rate will vary by lender, loan amount, and individual credit profile.

That $177 monthly gap isn’t random. It’s the price of a weaker credit profile — and Tim may not have even known his profile read that way until the rate came back.

That’s the problem with checking your credit score too late. By the time the number hits the screen, the decision has already been made.

What Is a Credit Score and How Does It Affect Your Rate?

A credit score is a three-digit number, typically ranging from 300 to 850, that represents how likely you are to repay borrowed money based on your past financial behavior. The most widely used model is the FICO Score, developed by the Fair Isaac Corporation. VantageScore is another common model, though FICO remains the dominant standard among major lenders.

The score itself isn’t an opinion. It’s a calculation — produced by running your credit history through a formula that weighs different financial behaviors and assigns them varying levels of importance.

What it is not: a measure of your income, your net worth, your intelligence, or your character. Two people with identical salaries can have credit scores that are 150 points apart. Two people with very different incomes can have nearly identical scores. The score is narrowly focused on one thing — your track record with credit — and it draws a hard line between people who look like reliable borrowers and those who don’t.

What Are the Five Factors That Build Your Credit Score?

Your FICO Score is calculated from five categories of information pulled directly from your credit report:

Payment history (35%) — This is the single largest factor. It captures whether you’ve paid your bills on time across every account — credit cards, loans, lines of credit. One missed payment doesn’t destroy a score, but a pattern of late payments, defaults, or accounts sent to collections does serious damage that takes time to work through. If you’ve just missed one, what actually happens in the first 30 days — and what to do immediately.

Amounts owed — credit utilization (30%) — This measures how much of your available revolving credit you’re currently using. If your combined credit card limits total $10,000 and your current balances total $6,500, your utilization is 65%. Most lenders prefer to see this number below 30%. High utilization signals financial pressure, regardless of whether you’re making minimum payments on time. If your card balance barely moves despite paying every month, that’s not a budgeting problem — it’s how minimum payments are designed. Understanding exactly how that utilization ratio suppresses your score — and what it costs on your next loan — is what this breakdown of credit utilization and loan rates covers in full. The reason balances persist despite consistent payments — keeping utilization elevated month after month — is explained in why minimum payments don’t work. The credit card minimum payment calculator shows how long a specific balance actually takes to clear — and how much of each payment disappears into interest.

Length of credit history (15%) — Longer histories generally produce stronger scores, because they give lenders more behavioral data to evaluate. This is why closing old accounts — even ones you don’t use — can sometimes work against you. It shortens your average account age.

Credit mix (10%) — Lenders like to see that you can handle different types of credit responsibly. A profile that includes both revolving credit (like credit cards) and installment loans (like auto loans or student loans) tends to score more favorably than one with only one type. Consolidating credit card balances into a personal loan does exactly this — it closes out revolving debt and replaces it with installment debt, which also removes the balance from your utilization ratio at the same time. See how the mechanics work and whether the APR math holds up.

New credit (10%) — Every time you apply for new credit, a hard inquiry is recorded on your report. Multiple hard inquiries in a short window can signal financial stress to lenders and put mild downward pressure on your score.

Together, these five factors create a profile that lenders use to make a fast, data-driven judgment about how much risk you represent.

Here’s something worth sitting with: most people who find out their rate was higher than expected already knew, somewhere, that their credit wasn’t perfect. What they didn’t know was the dollar value attached to that imperfection. The gap in Tim’s story isn’t a worst-case scenario. It’s a common one.

What Happens to Your Loan Rate When Your Credit Score Improves?

Moving your score up by even one tier typically drops your offered APR by several percentage points — and translates directly into hundreds or thousands of dollars in savings over the loan term.

Tim’s situation doesn’t have to be permanent.

If Tim brought his score from the 580–620 range up to 680–720 — a realistic shift over 12–18 months with consistent on-time payments and reduced utilization — the same $20,000 loan at the same lender would likely come back at an APR closer to 17–19% rather than 28.5%.

At 18% APR over 42 months:

- Monthly payment: ~$645

- Total interest: ~$7,102

That’s roughly $4,700 in savings compared to Tim’s current rate — without touching the loan amount or the term. From one tier shift.

The system that punishes a weak credit profile is the same system that rewards an improving one. The math works in both directions.

An improved score is also the moment to revisit existing credit card debt — borrowers who couldn’t qualify for a competitive personal loan rate a year ago may now be in a different tier. Here’s how to check whether the math on a personal loan consolidation now works in your favor.

What Does Your Credit Score Actually Control?

Every time you apply for a credit card, a personal loan, an auto loan, or a mortgage, a lender pulls your credit information and runs it through their underwriting process. They’re not going off gut instinct. They’re looking at signals — patterns in your financial behavior that tell them how risky it is to extend credit to you.

Your credit score is one of the first data points they see, and it shapes:

- Whether you get approved at all

- What interest rate you’re offered

- How much credit you can access

- What your monthly payment obligations end up being

This isn’t a soft filter. It’s a hard one. And the effect is felt well beyond personal loans. Your credit profile follows you across nearly every major financial decision you’ll make.

If you’ve already applied and been turned down, the next step isn’t to apply somewhere else — it’s to understand why the application failed and what to fix before reapplying.

Where Does Your Credit Score Follow You Beyond Loan Applications?

Most people associate credit scores with loan applications. The reach is wider than that.

| Situation | How your credit score affects it |

|---|---|

| Mortgage | Single biggest long-term impact — a tier difference can mean tens of thousands of dollars over 30 years |

| Auto loan | Same car, same dealership, same day — dramatically different monthly payment depending on credit tier |

| Credit cards | Determines approval, limit, and rate — weaker profiles get lower limits, making utilization harder to control |

| Apartment rental | Many landlords run credit checks; poor profiles result in rejection or a larger security deposit requirement |

| Utility accounts | Some providers require a deposit before establishing service below a certain credit threshold |

| Insurance premiums | Auto and homeowners insurers in most U.S. states use credit-based scoring as a pricing factor |

| Employment | Finance, government, and security clearance roles may review credit history as part of the hiring process |

The common thread: your credit profile is being evaluated in contexts you may not have anticipated, often without your active awareness.

Why Do Two Borrowers Get Such Different Rates on the Same Loan?

Lenders charge different rates because they are pricing risk — and your credit score is the single number that quantifies how risky you look before you say a word.

Going back to Andy and Tim — the $7,437 difference in what they paid wasn’t the lender penalizing one of them. It was the lender pricing risk accurately.

Lenders operate on a fundamental principle: the less predictable a borrower’s repayment behavior looks, the more it costs to lend to them. That cost gets passed directly to the borrower in the form of a higher interest rate. It’s a buffer against the statistical probability that some borrowers won’t repay in full.

This is why the credit score system exists. Before it, lending decisions were far more subjective — subject to the biases, assumptions, and inconsistencies of individual loan officers. A standardized numerical score created a more systematic way to evaluate risk across large volumes of applications quickly and consistently.

Is it a perfect system? No. But it operates on a clear, documented logic — and that logic can be understood, tracked, and navigated by anyone who takes the time to learn it.

When Do Most People Check Their Credit Score — and Why Does That Timing Work Against Them?

The most common triggers for checking a credit score are:

- Receiving a loan rejection

- Getting hit with an unexpected interest rate

- Facing repeated declines on credit applications

- Noticing an unexplained change in a monthly payment

These are all reactive moments. The checking happens after the outcome. And at that point, the hard inquiry has already been recorded on your report, the adverse action has already been issued, and the decision is already final.

Checking your credit score after the fact doesn’t rewind what happened. It just tells you why. If you’re in that position now, this breakdown of loan rejection factors walks through exactly what lenders flagged and what to address before you apply again.

What Do the Most Common Credit Score Assumptions Actually Cost You?

“Income is the main factor.” This is the most expensive misconception. A high income doesn’t override a troubled credit history in most underwriting models — income isn’t even part of the FICO calculation. Your credit profile acts as the initial gate. Income is considered only after you’ve already passed through it.

“All lenders evaluate the same way.” Different institutions use different scoring models and set different approval thresholds. The same applicant can be approved by one lender and declined by another. Knowing which credit tier you’re operating in tells you which products you’re realistically positioned for — before you apply and absorb the hard inquiry.

“A single missed payment won’t matter much.” Payment history is the most heavily weighted factor in your score — 35% under FICO. A payment 30 days late can produce a measurable drop, and the effect is most pronounced on profiles that were previously clean. The stronger your score going in, the more a single miss costs. (Here’s what the 30-day reporting threshold means in practice — and how to stay on the right side of it.)

“My score is fine because I haven’t been rejected.” Not being rejected doesn’t mean your profile is optimized. You may have qualified — but at a rate or limit that’s higher than what a stronger profile would have produced. The cost is still there. It’s just less visible than a rejection letter.

What’s the Difference Between a Credit Report and a Credit Score?

Your credit report is the full document — a detailed record of every account, payment, and inquiry. Your credit score is a compressed number calculated from what’s in that report.

Your credit report is the full document — a detailed record of every credit account you’ve ever held, every payment history, every inquiry, every public record. It’s maintained separately by each of the three major credit bureaus: Equifax, Experian, and TransUnion. These reports can differ from one bureau to another, because not all lenders report to all three.

Your credit score is derived from what’s in that report — a compressed numerical summary produced by running the report’s data through a scoring algorithm.

You can have a credit score that looks acceptable and still have problems on your underlying credit report that a lender will see — errors, duplicate accounts, incorrect balances, outdated negative items that should have aged off. The score reflects the report. If the report has inaccuracies, the score reflects those too.

Under the Fair Credit Reporting Act, every U.S. consumer is entitled to a free copy of their credit report from each bureau. All three bureaus now permanently offer free weekly access — you can pull your report from each bureau as often as once a week through AnnualCreditReport.com. That’s the place to start if you’ve never reviewed what your actual report contains.

How Do You Know Where You Stand Before It Costs You?

The first step is pulling your credit report and checking which score tier you currently occupy — before you apply for anything. That snapshot tells you what a lender will see, and it tells you whether there’s anything to fix.

That means not waiting for a rejection, a surprise rate, or an unexplained decline to prompt the first look at your credit profile. It means understanding where you currently sit in the credit tier system before you apply for anything. It means knowing whether there are errors or anomalies on your report that could be affecting how lenders see you — and having time to address them before they cost you.

Your credit profile is one of the few financial variables that lenders see before they see anything else. Understanding what’s in it isn’t a precaution reserved for people with credit problems. It’s a basic part of navigating financial products as an informed adult.

The numbers in Andy and Tim’s story aren’t outliers. They’re a realistic illustration of what the credit scoring system produces every day, for millions of people making ordinary financial decisions.

The difference is simply whether you know where you stand before the rate comes back — or after.

If you’ve been tracking your score but not seeing the improvement you expected, here’s why that happens — and what actually moves the needle.

Where to Start Based on Where You Are

Your balance is barely moving despite monthly payments → The issue is almost certainly interest rate, not payment consistency. See why minimum payments are designed to keep balances elevated before choosing a path forward.

Your score is in the Fair or Poor tier (below 670) → The fastest levers are: reduce credit utilization (pay down balances before statement closing date), make every payment on time for 6–12 months, and dispute any errors on your report. See the utilization-to-score cost breakdown.

You’ve been rejected for a loan → Don’t reapply immediately. A second hard inquiry makes the picture worse. Find out exactly what triggered the rejection and what to fix first.

This article is for informational purposes only and does not constitute financial advice. Credit score ranges and interest rate figures are used for illustrative purposes based on publicly available market data.