- Why seeing the math behind stagnant credit card debt isn't enough to fix it — and how the behavioral loop that forms around it quietly extends the problem for months or years.

- Who this hits hardest: the responsible payer who never misses a payment but gradually stops checking, loses intentionality, and watches the balance hold indefinitely.

- What the calculator below reveals about your actual payoff timeline — and why that number is the moment the loop either continues or finally breaks.

There’s a specific kind of financial exhaustion that doesn’t come from overspending or missing payments. It comes from doing everything right — and watching nothing change.

You pay every month. On time. The account is in good standing. And the balance looks almost exactly the same as it did three months ago.

A few dollars here. Maybe a hundred there. But the number barely moves. At some point you stop expecting it to. You pay the minimum, close the app, and move on. The debt starts to feel permanent — not a temporary problem you’re actively working through, but a fixture.

That’s not a discipline failure. It’s the predictable outcome of how credit card debt is designed to work — and what that design does to behavior over time.

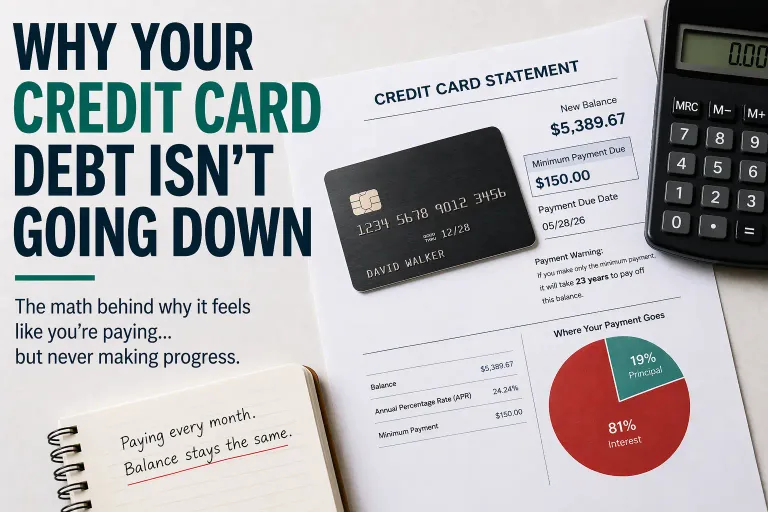

Why Credit Card Balances Barely Move

The mechanics are straightforward: your interest rate is applied to your balance every day before your payment reduces it. At 20% APR, a $5,000 balance generates roughly $83 in interest every single month — charged daily, before your payment even posts. If your minimum payment is $100, only about $17 is actually reducing your debt. The rest disappears into interest.

That $17 is the number the minimum payment structure is designed to produce. Not enough progress to feel real. Not enough to create a visible payoff arc. Just enough to keep the account current — and the balance generating interest.

As your balance slowly drops, your minimum shrinks with it. That sounds like progress. It isn’t. A lower minimum means even less goes toward principal. The timeline extends further, not shorter.

The full breakdown of how issuers calculate minimums, why the shrinking minimum is a trap rather than a reward, and what CFPB disclosures require issuers to tell you is covered in why minimum payments don’t work. What matters here is what that structure does to the person on the other side of it.

See What Your Balance Is Actually Costing You

Before the rest of this article, run your own numbers. Enter your current balance, APR, and what you’ve been paying each month.

Credit Card Payoff Calculator

⚠ Estimates use a fixed monthly payment model. Actual timelines vary based on minimum payment recalculations and card terms.

That payoff timeline — the number that just appeared — is what the system produces by default if nothing changes. Most people have never seen it written down.

That number is also where the behavioral problem begins.

The Loop That Keeps People Stuck

Seeing 12 years, 17 years, $7,000 in interest on a $5,000 debt — that creates a window. A moment where the problem is concrete enough to act on.

For most people, that window closes.

Not because they don’t care. Because the system gives them no useful feedback for what to do next. Here’s what happens instead:

Pay → see almost no visible progress → quiet frustration → start avoiding statements → pay the minimum and close the app → balance holds or drifts up → loop repeats

Each cycle, the behavioral engagement that’s actually required to break out fades a little more. The payments continue — but the intentional tracking, the calculation, the decision-making? That disappears. And that’s exactly when balances tend to creep back up.

This is the part that doesn’t show up in minimum payment math. It’s not just that the structure is slow — it’s that the slowness erodes the conditions that change the outcome.

When effort produces no visible result, the brain disengages. That’s not irresponsibility. It’s a completely predictable response to a feedback system that was never designed to give you accurate signals about your progress.

(If a payment slips in that window, here’s what the 30-day timeline looks like — and what to do before it hits your credit report. If the pressure compounds to the point where stopping payments entirely starts feeling like a way out, the full consequence sequence — and what’s available before it reaches that point — is covered here.)

Understanding the loop changes the frame entirely. It’s not a discipline problem. It’s a design problem. And the design isn’t accidental.

Why the System Is Built to Keep You in This Loop

Credit card minimum payment structures are built to serve the issuer. A cardholder who carries a $5,000 balance for five years generates significantly more revenue than one who pays it off in six months. Long repayment timelines are the outcome the structure is optimized to produce.

But what makes the design effective isn’t just the math — it’s the psychological cover it provides. The account is current. Nothing is technically wrong. There’s no urgent signal. The balance feels temporary: it’s been there for months, but it’ll go down eventually.

Meanwhile, the minimum shrinks as the balance (barely) drops. A lower minimum feels like good news. It isn’t. It means even less goes toward principal each cycle. The timeline lengthens.

The elevated balance also keeps your credit utilization high — which suppresses your credit score and raises the rate you’d be offered the next time you need to borrow. The debt problem quietly becomes a borrowing cost problem.

The CFPB’s minimum payment warning — legally required on every statement — shows exactly what this produces over time. Most people scroll past it. The structure works whether they read it or not.

This isn’t a conspiracy. It’s a business model. Understanding it doesn’t require outrage — just clarity. You’ve been following a structure that was never designed to help you get out of debt. Now you can stop.

What Actually Changes the Outcome

Breaking the loop requires one of three changes — not eventually, but this month.

1. Pay More Than the Minimum

The simplest lever. When you pay above the minimum, the surplus goes almost entirely to principal. Less principal means less interest next cycle. The suppression compounds — faster than most people expect.

On a $5,000 balance at 20% APR: bumping your monthly payment from the minimum to $200 could pay off the debt in about 2.5 to 3 years — compared to nearly two decades on minimums. Even an extra $50 a month reshapes the math meaningfully. It’s not about dramatic sacrifice. It’s about taking the payment pace out of the issuer’s hands and putting it back in yours. If you’re not sure where that extra payment comes from, start with the wants category — in a 50/30/20 budget, any payment above the minimum belongs in the 20% savings and debt paydown bucket, not the needs floor. That reclassification alone often reveals room that wasn’t visible before. If a budget isn’t in place yet, building one from scratch is what makes that room visible — or shows clearly that the gap is structural before you try to find dollars that aren’t there.

2. Reduce the Interest Rate

If the rate comes down, more of every payment reaches principal — without paying more. Call your issuer directly and request a reduction. It costs nothing to ask, especially with a clean payment history. Issuers often prefer adjusting a rate slightly over losing the account to a balance transfer.

Your rate isn't fixed forever — it's tied to your credit profile. A stronger credit score can significantly lower the rates you're offered, which directly reduces how much of your payment goes toward interest each month. For people trying to build that profile without going back into revolving debt, there are credit-building tools that don't require carrying a balance.

3. Restructure the Debt Entirely

For balances where the interest rate makes meaningful progress nearly impossible, restructuring is often the turning point. Balance transfer cards (0% promotional APR for 12–21 months) and debt consolidation loans (fixed-rate installment loans at lower rates than revolving credit) both convert an open-ended situation into a defined payoff plan.

If you’re weighing these two options, Debt Consolidation vs Balance Transfer compares real payoff numbers for both — and a clear framework for which one saves more depending on your balance and repayment speed. For a detailed look at how a personal loan handles credit card consolidation specifically — including origination fee math, the APR comparison you need to run first, and why paid-off cards are the most common failure point — this guide covers it end to end.

Restructuring also removes revolving debt from your utilization calculation entirely — which can lift your score and lower the rate you’re offered on any future borrowing. See how utilization affects what lenders charge you →

Financial Assistance

Sometimes the Issue Is Bigger Than the Card

If managing this debt alongside other financial pressures has become overwhelming, Financial Help Finder searches available grant and assistance programs matched to your situation — free, no purchase required.

See What's Available →Where to Start Based on Where You Are

You’ve been paying minimums for 6+ months with no visible progress → The calculator above showed you the real timeline. The behavioral loop is already running. The next move is picking one of the three options above and acting on it this month — not next month.

Your balance is $5,000 or below → A balance transfer to a 0% intro APR card is likely the fastest, cheapest path. The fee (3–5%) is typically less than one month of interest. Compare balance transfer vs. consolidation loan options here.

Your balance is over $10,000 or on multiple cards → A debt consolidation loan converts unpredictable revolving debt to a fixed-rate installment loan with a defined payoff date. See whether the APR math works in your favor.

This article is for informational purposes only and does not constitute financial, legal, or tax advice. Consult a qualified financial professional before making financial decisions.