- Why simple and compound interest produce radically different outcomes — and how the same mechanism that grows your investments can silently double your debt.

- Who pays the highest price for this gap — and why most borrowers only discover which type they're dealing with after they've already signed.

- What the actual numbers show across three real scenarios — and how to use the simulator below to see the exact dollar difference on your own situation.

Most people find out the hard way.

They take out a loan, carry a credit card balance, or open an investment account—and years later, the numbers don’t add up the way they expected. Either they paid far more than they planned, or their money grew faster than they thought possible.

The difference almost always comes down to one thing: what type of interest was working on their money.

Understanding the difference between simple and compound interest can help you avoid costly debt and make better investing decisions. This article breaks down both—with real numbers—so you know exactly what you’re dealing with before you sign anything.

What Is the Difference Between Simple and Compound Interest?

Simple interest is calculated only on the original amount you borrowed or invested—the principal. It grows in a straight line.

Compound interest is calculated on the principal plus any interest that has already accumulated. That means interest earns interest. Over time, it grows exponentially—not linearly.

For borrowers, that distinction is the difference between a manageable loan and a debt that feels like it never shrinks. For investors, it’s the difference between steady growth and wealth that accelerates on its own.

| Feature | Simple Interest | Compound Interest |

|---|---|---|

| How it’s calculated | On original principal only | On principal + accumulated interest |

| Growth type | Linear | Exponential |

| Cost (for debt) | Lower and predictable | Higher over time |

| Benefit | Borrowers | Investors and lenders |

| Predictability | High | Lower (depends on time and compounding) |

How Can You Tell Which Type of Interest You’re Dealing With?

Most people forget to ask this question—and it matters.

If interest is only ever calculated on your original balance, you’re dealing with simple interest. Your total cost is fixed from day one.

If your balance keeps rising even when you make payments, or your investment seems to accelerate over time, that’s compound interest.

In the real world:

- Credit cards almost always use compound interest. According to the Consumer Financial Protection Bureau (CFPB), most issuers compound interest daily using a daily periodic rate derived from your APR—so every day you carry a balance, interest is calculated on the full amount owed.

- Some personal and auto loans use simple or amortized interest structures, where payments are scheduled over time but don’t compound like credit cards.

- Savings accounts and investment accounts typically use compound interest, which works in your favor.

When you’re reviewing a loan offer or credit card agreement, look for terms like “daily periodic rate,” “daily compounding,” or “average daily balance.” Those phrases tell you compound interest is involved.

Quick test:

- If your balance grows even when you’re not making new purchases → it’s compound interest

- If your total repayment amount is fixed from the start → it’s simple interest

- If interest is calculated daily or monthly on a changing balance → it’s compound

How Much More Does Compound Interest Cost Compared to Simple Interest in Real Examples?

Let’s put real numbers to this so you can see the actual cost difference.

Example 1: $5,000 Credit Card Balance (Compound Interest)

Say you carry a $5,000 balance on a credit card with a 24% APR—which is close to the current national average. According to the Federal Reserve, the average credit card interest rate in the U.S. has exceeded 20% in recent years.

At 24% APR compounded daily, if you only make minimum payments each month (typically structured as roughly 1% of your principal plus interest charges — around $150 initially on a $5,000 balance), here’s what happens:

| Amount | |

|---|---|

| Time to pay off | ~17–19 years |

| Total interest paid | ~$6,000–$7,000 |

| Total repayment | ~$12,000 |

| Amount originally borrowed | $5,000 |

You borrowed $5,000—but you could end up paying more than double. That’s what compound interest does when it’s working against you.

If you want to understand why credit card balances grow this way, read our breakdown of why credit card debt doesn’t go down. And the same balance that’s compounding is also elevating your credit utilization — which suppresses your score and raises the rate you’re offered on future debt. See how utilization affects your actual loan costs →

Example 2: $5,000 Simple Interest Loan

Now take the same $5,000 borrowed as a personal loan at a fixed simple interest rate of 10% over 3 years.

- Monthly payment: approximately $161

- Total interest paid: roughly $800

- Total repayment: about $5,800

The cost is predictable. It doesn’t snowball. You know exactly what you owe from day one.

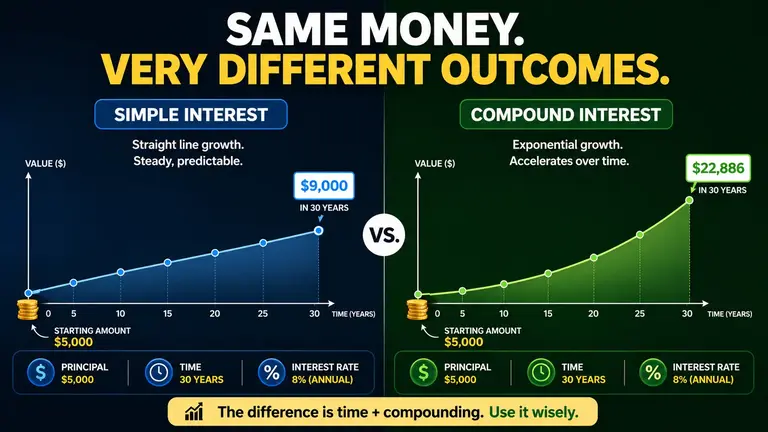

Example 3: $5,000 Invested (Compound Interest Working For You)

Now flip it. You invest $5,000 in a low-cost index fund averaging 8% annual returns, compounded annually.

| Year | Balance |

|---|---|

| 5 | ~$7,347 |

| 10 | ~$10,795 |

| 20 | ~$23,305 |

| 30 | ~$50,313 |

You didn’t add another dollar. Compound interest did the work. This is why long-term investing works—even without constant contributions—and why you can learn how consistent investing builds wealth over time. Over 30 years, your $5,000 turned into over $50,000.

Same concept—opposite outcome depending on which side of it you’re on.

Key takeaway: The same interest system that grows your investments can also double your debt—depending on which side you’re on.

Interactive Calculator

Simple vs. Compound Interest Simulator

Adjust the numbers to see how simple and compound interest diverge over time. The gap is the story.

Simple Interest

—

Compound Interest

—

Difference

—

Is Compound Interest Better Than Simple Interest?

It depends on which side of it you’re on.

For borrowers: Simple interest is better. Your cost is fixed and doesn’t accelerate. You know exactly what you owe and when you’ll be done.

For investors and savers: Compound interest is better. Each period’s gains compound on top of the last, so returns accelerate the longer you stay invested.

Compound interest isn’t inherently good or bad—it’s a mechanism. What matters is whether it’s working for you or against you.

The short version: borrow simple, invest compound.

What Is the Rule of 72 (And Why It Matters)?

The Rule of 72 is a commonly used financial shortcut for estimating how long it takes compound interest to double your money.

The formula: 72 ÷ your interest rate = approximate years to double

| Interest Rate | Years to Double |

|---|---|

| 4% | 18 years |

| 6% | 12 years |

| 8% | 9 years |

| 10% | 7.2 years |

| 12% | 6 years |

| 24% (credit card APR) | 3 years |

It also works in reverse for debt. At 24% APR, a credit card balance could theoretically double in about 3 years if left unpaid—which explains how quickly balances spiral.

The Rule of 72 doesn’t require a calculator. It’s a quick way to grasp the power of compounding at a glance.

Why Does the Difference Between Simple and Compound Interest Matter for Your Money?

If you’re carrying high-interest debt, compound interest is working against you every day. The longer the balance stays, the more you pay. Paying it down aggressively—or consolidating at a lower rate—directly cuts the compounding effect. Seeing exactly how much that monthly interest cost represents relative to your take-home is the work of a budget — building one from scratch is where the debt line becomes a real number inside the full monthly picture.

If you’re investing, compound interest is your most reliable long-term tool. It doesn’t require perfect picks or market timing—just time. The earlier you start, the more compounding periods you get.

If you’re deciding whether to invest or pay off debt first, read our full guide on whether you should pay off debt or invest first.

When Does Each Type Apply to Your Money?

Most finance content explains the mechanics—but stops before telling you which products actually use each type. Here’s where each one shows up in practice.

Mortgages

Mortgages in the U.S. typically use amortized interest, which is structured similarly to simple interest. Each monthly payment covers both principal and interest, and the interest portion is calculated on the remaining principal balance—not on accumulated interest. That means a $300,000 mortgage at 7% doesn’t compound the way a credit card does.

What changes over time is the allocation: early payments go mostly to interest, later payments mostly to principal. But at no point is interest added to your principal and then charged again. This is why mortgage balances actually go down when you make consistent payments.

Credit Cards

As covered above, credit cards compound daily. The APR is divided by 365 to create a daily periodic rate, which is applied to your full balance every single day—including previously accumulated interest. This is why a $5,000 credit card balance at 24% APR can grow to over $12,000 if you only make minimum payments.

Carrying a balance past the grace period is one of the most expensive things you can do with debt. Even a few months allows compounding to build momentum. It also keeps your credit utilization elevated — which means the next loan you take out gets a higher rate before you’ve even applied. See how utilization raises your borrowing costs →

Savings Accounts and CDs

Standard savings accounts and certificates of deposit (CDs) use compound interest—typically compounded daily or monthly, credited monthly. Here, compounding works in your favor. A high-yield savings account at 4.5% APY compounds daily, so earned interest starts earning interest immediately.

One thing to note: APY (Annual Percentage Yield) already accounts for compounding—it reflects the effective annual return after compounding, while APR does not. When comparing savings products, always compare APY to APY.

Investment Accounts

Index funds and brokerage accounts don’t use a set interest rate—returns vary by market performance. But the compounding effect still applies: dividends are reinvested, gains generate further gains, and the portfolio grows over time. This is the same mechanism as compound interest, applied to variable returns instead of a fixed rate. It’s why long-term investing works even without constant contributions.

Student Loans

Federal student loans typically use simple interest, accrued daily on the outstanding principal. Interest doesn’t capitalize (get added to principal) unless you exit a grace period, leave deferment or forbearance, or enter certain repayment plan transitions. Private student loans vary—some compound, some don’t. Always check before signing.

The Pattern

| Product | Interest Type | Works For/Against You |

|---|---|---|

| Credit cards | Compound (daily) | Against |

| Mortgages | Amortized (simple-like) | Predictable |

| Savings accounts | Compound (daily/monthly) | For |

| Personal loans | Simple | Predictable |

| Student loans (federal) | Simple | Predictable |

| Investment accounts | Compound returns | For |

Knowing which category each product falls into changes how you evaluate offers, prioritize payoff, and set savings goals. The same question—what type of interest is working here?—applies whether you’re reviewing a loan offer, opening a new account, or deciding where to put extra cash.

What’s the Key Takeaway About Simple vs. Compound Interest?

Simple and compound interest are the same concept working in opposite directions depending on context.

Before you borrow, ask how interest is calculated. Before you invest, find vehicles where compounding works in your favor.

Most people don’t lose money because they don’t understand interest—they lose money because they don’t realize when it’s working against them.

Sources: Consumer Financial Protection Bureau (CFPB) — credit card interest calculation methods; Federal Reserve — average U.S. credit card interest rate data; Investopedia — Rule of 72 explanation and compound interest definitions.