- Why an emergency fund is the infrastructure that stops one bad month from becoming six bad months — and why most people don't have one for structural reasons, not personal ones.

- Who gets hit hardest when the fund doesn't exist — and why the income level most people assume is "safe enough" is often the one most exposed to a single unexpected expense.

- How to calculate a real target amount based on your own numbers, where the right place to keep it is, and what counts as a legitimate emergency — so the fund doesn't quietly disappear.

The car won’t start. It needs a timing belt. The shop says $900.

That $900 isn’t unusual. It isn’t catastrophic. But for 37% of U.S. adults, it means borrowing — a credit card charge at 24% APR, a personal loan, a call to family. According to the Federal Reserve’s 2025 Report on the Economic Well-Being of U.S. Households, more than one in three American adults cannot cover a $400 emergency with cash without selling something or going into debt — a figure that has held steady for three consecutive years.

The problem isn’t the $900. It’s that there was no buffer between the expense and the damage.

That’s what an emergency fund is: not a savings goal to work toward eventually, but infrastructure — a circuit breaker that keeps one financial shock from cascading into missed payments, new debt, and months of recovery.

This guide covers how to calculate your target, where to keep the money, and how to start — including if you’re currently carrying debt or have nothing left at the end of the month.

Not sure if you’re in a position to save right now? If bills are consuming everything, skip to Where to Start Based on Your Situation — that section covers your scenario specifically, including how to find assistance programs if you’re not yet at the savings stage.

Why Don’t Most People Have an Emergency Fund — and Is It Really a Discipline Problem?

The standard explanation is lack of discipline or willpower. The accurate explanation is structural.

Income Volatility, Not Just Income Level

Irregular income makes consistent saving structurally harder — not because people spend irresponsibly, but because the surplus that savings requires doesn’t reliably exist. A gig worker, an hourly employee with variable shifts, or someone on commission doesn’t have a predictable monthly surplus to redirect. Part-time workers represent approximately 17% of total U.S. employment, according to the Bureau of Labor Statistics Current Population Survey (2024). For these workers, “save a fixed amount each month” ignores how their income actually works.

The Cost of Existing Debt

Monthly minimum payments absorb the cash flow that would otherwise become savings. The fund never gets started because debt service gets first claim on every paycheck. If $400 per month goes to minimums before any other decision is made, the math of saving becomes genuinely constrained — in ways that discipline alone can’t fix. Why minimum payments don’t work explains exactly how this trap compounds over time.

No Automatic Mechanism in Place

Perhaps the most honest explanation: most people don’t have an emergency fund because there is no system that builds one automatically. There was no decision made against having one — it simply never got set up. The step-by-step plan below is about building the system. Motivation usually follows once the balance starts to grow.

How Do You Build an Emergency Fund Step by Step?

Step 1 — Calculate Your Actual Target

The target is not a round number someone else chose. It’s a function of two inputs: your monthly essential expenses multiplied by the number of months of coverage you want.

Essential expenses are the costs you’d still pay during a real emergency — the ones you can’t cut:

- Rent or mortgage

- Utilities

- Groceries

- Insurance premiums (health, car, renters or home)

- Minimum debt payments

- Transportation to work

What is NOT included in essential expenses: subscriptions, dining out, entertainment. In a real emergency, those get cut. Your target should reflect actual survival costs, not current lifestyle spending.

On coverage months, here’s a practical framework:

- 3 months — the minimum viable floor. Covers most job loss scenarios where re-employment happens within a quarter.

- 6 months — the standard benchmark for single-income households and variable-income workers. The Consumer Financial Protection Bureau uses 3–6 months as its baseline recommendation, with more coverage recommended for households with irregular income.

- 12 months — appropriate for the self-employed, freelancers, or anyone on commission-only income where finding new work or clients could take longer.

To calculate your personal number: add up your essential monthly expenses, then multiply by your chosen coverage months. That is your target — not a guess, not someone else’s average.

Emergency Fund Calculator

Calculate Your Emergency Fund Target

Include rent or mortgage, utilities, groceries, insurance, and minimum debt payments. Exclude subscriptions, dining out, and entertainment.

How much can you realistically set aside each month toward this fund?

Estimates only. Results assume consistent monthly contributions and do not account for interest earned.

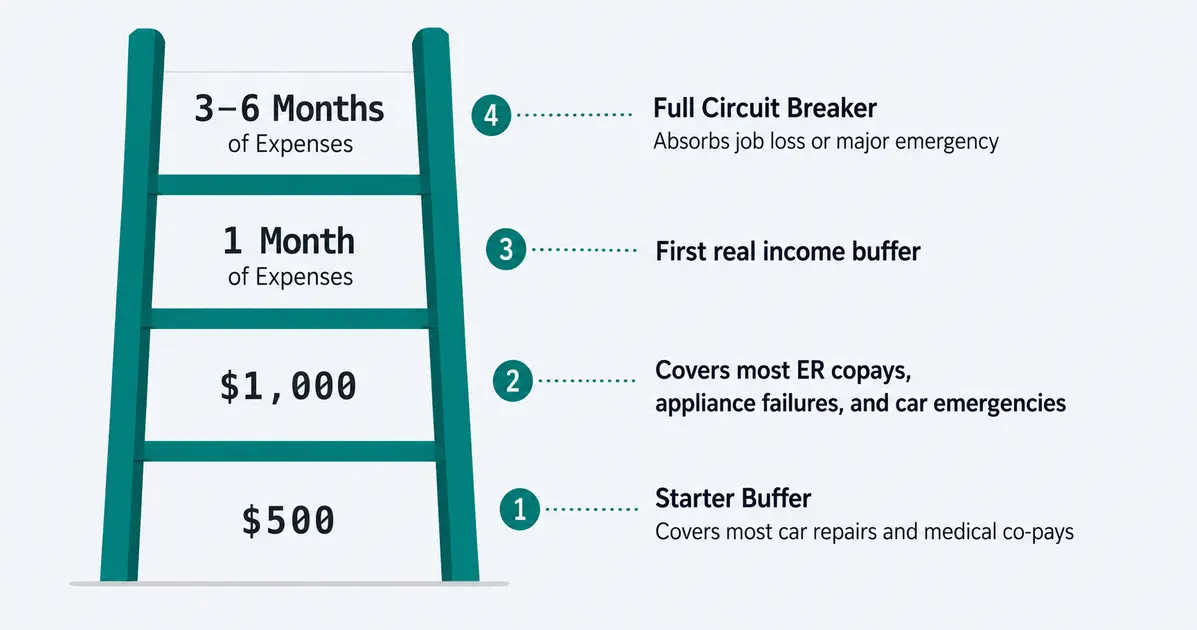

Step 2 — Start With $500, Not Six Months

Most people abandon the goal before they start because the number is intimidating. A 3-month fund for the median household requires saving roughly $15,000. That’s not a starting goal. That’s a finish line.

Start with $500.

A Bankrate survey found that 59% of Americans couldn’t cover a $1,000 emergency expense from savings alone — which means $500 already puts you ahead of more than half the country. More practically: a $500 buffer handles the most common single-incident emergencies (a car repair, a medical co-pay, a broken appliance). It doesn’t replace a full fund, but it stops the smallest shocks from immediately becoming debt.

Milestone progression: $500 → $1,000 → 1 month of expenses → full target.

Each milestone is a real threshold, not just a progress marker. A $1,000 fund covers the majority of emergency room copays, most car repairs, and most appliance failures. You’re not just making progress — each step closes off a category of financial damage.

Once you reach $500, set the next milestone. Progress builds momentum in a way that staring at a distant finish line never does.

Step 3 — Where to Keep It

The fund has one job: be available when you need it, without friction, and without being so accessible that it quietly disappears into everyday spending.

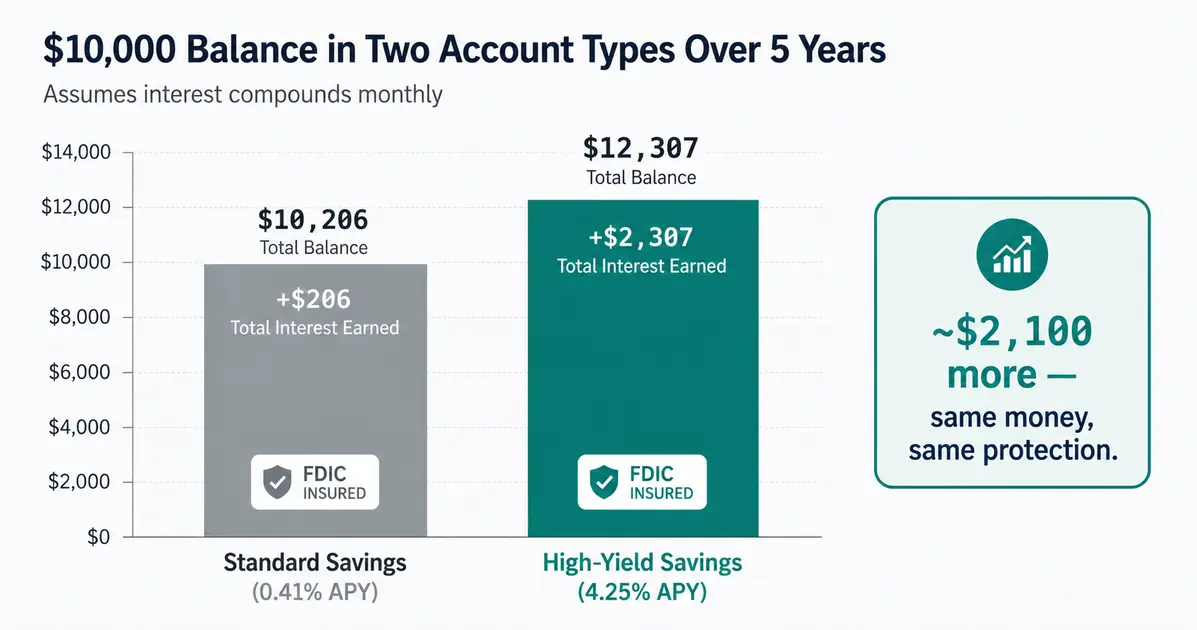

The right vehicle for this is a High-Yield Savings Account (HYSA).

A high-yield savings account is a savings account at an online bank or credit union that pays significantly more interest than a standard savings account. The math is straightforward:

| Account type | APY | Annual interest on $10,000 |

|---|---|---|

| Standard savings (national avg, FDIC Jan. 2025) | 0.41% | ~$41 |

| High-yield savings account (competitive, 2025) | 4.00–4.25% | ~$400–$425 |

That’s roughly $360–$380 more per year — on the same balance, with the same FDIC insurance, just by choosing the right account type.

Why an HYSA is the correct vehicle: it’s liquid (accessible within 1–2 business days), FDIC-insured, earns meaningful interest, and kept separate from your checking account — which matters more than it sounds. When emergency money lives alongside spending money, it quietly disappears on things that aren’t emergencies.

What to avoid: a checking account (too accessible, earns nothing), a CD (locked behind penalties when you need it most), or a brokerage account (subject to market loss at exactly the wrong time).

Step 4 — Automate the Transfer

Automation converts a one-time decision into a recurring system. And recurring systems are how emergency funds actually get built.

Set a recurring transfer from your checking account to your HYSA — scheduled for the same day as payday, before any discretionary spending occurs. The amount matters less than the consistency: $25 per week, $50 every two weeks, $100 per month — all of these work. At $100 per month, a $3,000 target takes 30 months. At $200 per month, it takes 15. The calculator above gives you the exact timeline for your numbers.

Most online banks allow you to schedule recurring transfers in under five minutes. Once it’s set up, the fund builds in the background without requiring ongoing willpower or decision-making. That’s the entire point.

Step 5 — Define What Counts as a Real Emergency

Without a clear definition, the fund depletes on things that are not emergencies. This is one of the most common ways well-funded accounts quietly drain over time.

Legitimate emergencies:

- Job loss or sudden income disruption

- Medical or dental expense not covered by insurance

- Essential car repair needed to maintain employment

- Home repair that affects habitability — heat, plumbing, roof

- Emergency travel for a genuine family crisis

Not emergencies (common mistakes):

- A sale on something you wanted to buy anyway

- A planned trip or event

- A tax bill — taxes are predictable and should be budgeted separately, not treated as surprises

- Credit card minimum payments — these belong in the regular budget (in the 50% needs bucket under the 50/30/20 framework), not the emergency fund

The rule of thumb: if the expense could have been predicted and planned for, it should not come from the emergency fund. Every withdrawal for a non-emergency leaves the fund one real emergency short. The definition protects the fund’s purpose.

Should You Pay Off Debt or Build an Emergency Fund First?

This question comes up constantly, and it deserves a direct answer — not a “it depends” non-answer.

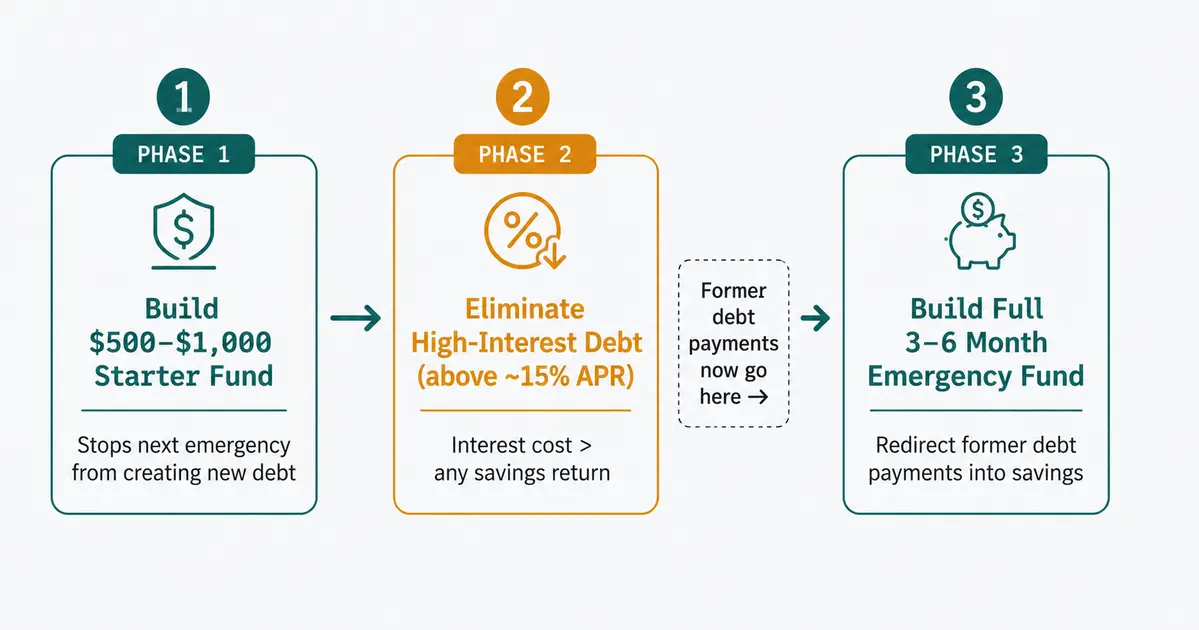

Build $500–$1,000 first, regardless of debt level. Without any buffer at all, the next unexpected expense goes straight back onto the credit card, erasing whatever debt progress you’ve made. The starter fund prevents debt from growing while you’re trying to pay it down. Whether you’re in the debt phase or the savings phase, a monthly budget built from scratch makes the sequencing decision concrete — it shows the current balance between income, essential costs, debt payments, and surplus, so the right next step is clear rather than a matter of guesswork.

Then address high-interest debt. Credit card debt above roughly 15% APR should come next. The interest cost of carrying that debt almost certainly exceeds what any savings account returns. The pay off debt or invest — the math guide walks through the calculations, and debt snowball vs. avalanche covers both payoff strategies in detail.

Then build the full fund. Once high-rate debt is cleared, the cash flow that was going to interest can now go directly into the emergency account — and it builds faster than before.

Lower Your Debt Cost First

If high-interest debt is what's preventing you from saving, a lower-rate personal loan consolidates what you owe into a single monthly payment — reducing what bleeds out each month and freeing up cash flow to start the fund.

Check personal loan rates →Can't Save Yet?

If building even a starter fund feels impossible because debt or bills are consuming the entire budget, this tool searches available assistance programs matched to your situation — free to check.

Find financial assistance →Where to Start Based on Your Situation

You have high-interest debt

Get $500 into a separate savings account first, then aggressively pay down the debt using snowball or avalanche. Once cleared, redirect those former payments directly into the emergency fund.

You are debt-free or carrying low-interest debt

Use the calculator above to set your target. Automate a recurring transfer to your HYSA starting this week. The amount matters less than the consistency.

Bills are consuming everything right now

Before focusing on savings, find out what assistance is available. Many households qualify for utility programs, food assistance, and healthcare subsidies they're unaware of. Reducing existing expenses creates the cash flow that makes saving possible.

Find available programs →Emergency Fund FAQs

How much should I have in an emergency fund?

The standard benchmark is 3–6 months of essential living expenses. Single-income households, variable-income earners, and the self-employed should target the higher end — 6–12 months. Calculate essential monthly expenses (rent, utilities, groceries, insurance, minimum debt payments) and multiply by your target months. The result is a personal number, not a round figure someone else chose.

What counts as a real emergency?

Job loss, unexpected medical or dental bills, essential car repairs needed to maintain employment, home repairs that affect habitability, and emergency travel for a genuine family crisis. A sale, a planned purchase, a vacation, or a credit card bill are not emergencies. The working rule: if the expense could have been predicted and planned for, it should not come from the emergency fund.

Should I build an emergency fund or pay off credit card debt first?

Build a $500–$1,000 starter fund first. Without any buffer, the next unexpected expense goes straight back onto the credit card, erasing debt progress. Then prioritize high-interest debt (above roughly 15% APR) before building the full fund — the interest savings exceed anything a savings account returns. Once high-rate debt is cleared, redirect those payments into the fund.

Where is the best place to keep an emergency fund?

A high-yield savings account at an online bank or credit union — separate from your everyday checking account. It should be FDIC-insured and accessible within 1–2 business days. Avoid a checking account (too accessible), a CD (locked), or a brokerage account (market risk when you can least afford it).

Is a high-yield savings account better than a regular savings account for this?

Yes, significantly. Standard savings accounts pay roughly 0.41% APY (FDIC, Jan. 2025). Competitive HYSAs pay 4.00%–4.25% APY — more than 10× more on the same balance. On a $10,000 emergency fund, that's roughly $360–$380 more per year in interest earned with no added risk. Both are FDIC-insured. (Note: HYSA rates are variable and tied to the Fed funds rate — check current rates before opening an account.)

What if I use the emergency fund — do I start completely over?

No. A fund that gets used did its job — it absorbed a shock that would otherwise have gone on a credit card. Replenish it the same way you built it: automate a recurring transfer and rebuild incrementally. Resume contributions as soon as the immediate situation stabilizes. The goal is to restore the balance, not to feel like you're starting from nothing.

How long does it take to build a 3-month emergency fund on an average income?

U.S. households spend an average of approximately $5,111 per month on essential expenses, derived from BLS Consumer Expenditure Survey data (2024). A 3-month fund at that level is roughly $15,333. At $200 per month: about 77 months. At $500 per month: about 31 months. At $1,000 per month: about 15 months.

What those numbers miss: a $1,000 fund — reachable in 5 months at $200 per month — already covers the most common single-incident emergencies. You're not waiting 77 months to have meaningful protection. You're 5 months from a fund that handles most real-life emergencies, and the full fund is the ceiling, not the floor. The calculator above gives you the exact timeline for your numbers.

What’s the Point of an Emergency Fund and Why Does It Matter?

The emergency fund isn’t about having a large number in a savings account. It’s about breaking the link between an unexpected expense and financial damage. $500 breaks that link for most common emergencies. $1,000 breaks it for most. A full fund breaks it for almost anything.

Pick the number that’s one step ahead of where you are right now, and automate a transfer this week. The size of the number matters less than the fact that it’s growing.