- The feeling that drives this search is real — overwhelming debt with no clear exit. But stopping payments doesn't pause the problem; it starts a sequence of consequences most people don't see coming until they're locked in.

- What happens: a late fee and penalty APR hit within 30 days. By 180 days, the account is charged off and sold to collectors — and the damage sits on your credit report for seven years, per CFPB guidance.

- What most people don't know: hardship programs, nonprofit credit counseling, and consolidation loans are all available before the point of no return — and any one of them can stop the bleeding without the long-term credit wreckage.

Which situation are you in?

- Still current on payments, but barely making it → Hardship programs and forbearance exist. Call your issuer before you miss the first payment. Jump to: What Options Exist Before You Reach That Point?

- Already 30–90 days behind → You still have options. Debt management plans and consolidation loans are available at this stage. Jump to: What Options Exist Before You Reach That Point?

- Severely delinquent or already in collections → The decision shifts to settlement vs. consolidation — a different calculation covered in our guide to Debt Settlement vs. Consolidation.

If you’re searching this, you probably know what it’s like to let the calls go to voicemail. To feel vaguely sick when the mail arrives. To do the math one more time and still not see a way through. That experience is not weakness — it’s what happens when the options feel invisible. This article makes them visible.

The consequences of stopping payments are real and worth knowing in full — they’re covered below in detail. But so are the exits. And the exits exist at stages most people assume are already too late.

What Actually Happens When You Miss Payments?

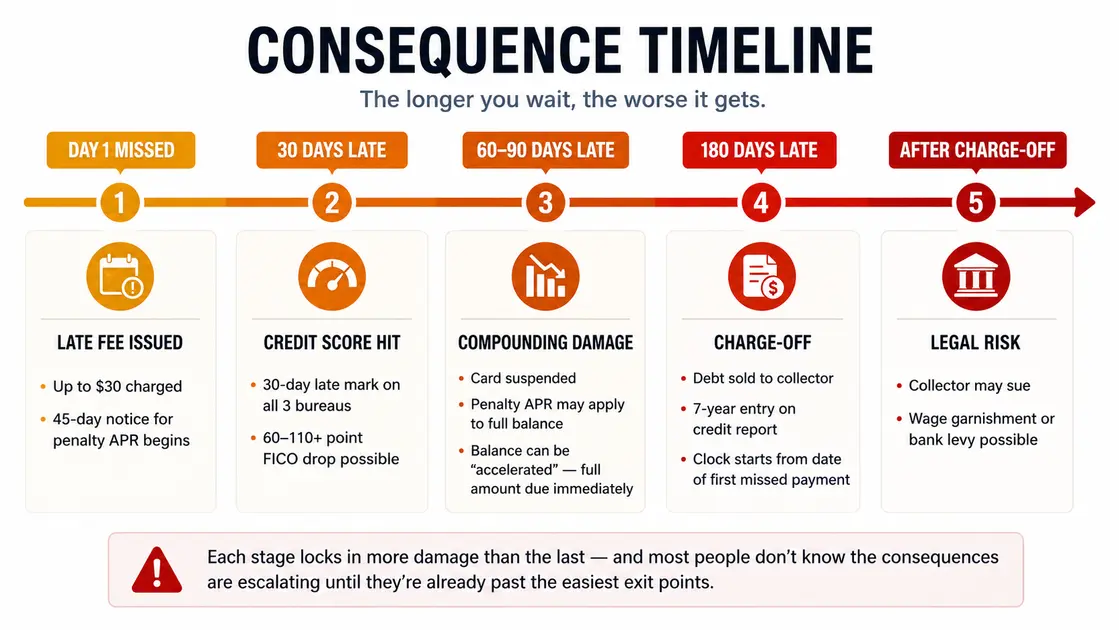

Most people imagine stopping payments as a pause — a way to catch their breath. What it actually starts is a sequence, and each stage in that sequence locks in more damage than the last.

30 Days Late

The clock starts the moment you miss your due date, but the first formal consequence hits at 30 days.

Your card issuer will charge a late fee. Under the Credit CARD Act, first-time late fees are capped at $30, and a second missed payment within six billing cycles allows a charge of up to $41. That’s the least of your concerns.

More damaging is what happens to your interest rate. Most major issuers can raise your APR to a penalty rate on new purchases after a single missed payment — with 45 days advance notice, as required under the Credit CARD Act. According to the CFPB, penalty APRs commonly reach up to 29.99%. If you reach 60 days past due, that penalty rate can then be applied retroactively to your existing balance as well. If you were carrying $8,000 at 22% and the penalty rate kicks in at 29.99% on the full balance, your monthly interest cost jumps meaningfully — on the same amount you already owed.

Then there’s the credit report impact. A 30-day late payment is reported to all three major bureaus. According to myFICO, a single 30-day late on an otherwise clean file can drop a FICO score by 60 to 110 points or more depending on your starting score — higher-score profiles (750+) tend to see the steepest drops. For context, that can push someone from “good” credit into “fair” territory overnight — affecting their ability to qualify for loans, apartments, or even certain jobs.

60–90 Days Late

At this stage, the situation compounds in multiple directions at once.

The late fees accumulate on top of a balance that’s now accruing at the penalty APR. Your credit score takes additional damage — 60-day and 90-day lates are weighted more heavily in FICO scoring models than the original 30-day mark. Think of each tier as a separate, increasingly severe entry on your report.

Issuers typically suspend the card, making it unusable, and begin internal collections outreach — calls, letters, sometimes email. Some issuers at this stage can “accelerate” the debt, meaning the full outstanding balance becomes due immediately rather than in future monthly installments. Most borrowers don’t know this clause exists in their cardholder agreement until they’re facing it.

120–180 Days Late

This is the point of no return for most accounts. At approximately 180 days past due — six months — the creditor writes the debt off as a loss. This is called a charge-off, and the CFPB is explicit that it does not mean the debt disappears. It means the creditor has reclassified it internally and will typically sell it to a third-party debt collector for pennies on the dollar.

Once purchased by a collector, the Fair Debt Collection Practices Act (FDCPA) governs how they can contact you — but they can and will. Under the Fair Credit Reporting Act (FCRA), both the charge-off and the original delinquency are removed seven years from the charge-off date — which is 180 days after first delinquency, meaning effectively 7.5 years from your first missed payment. The clock does not restart when the debt is sold to a collector.

Lawsuits and Wage Garnishment

If a collector obtains a court judgment against you, they may pursue wage garnishment — the percentage they can take varies by state — or a bank levy, which freezes and draws from your checking account.

The one protection worth knowing: every state has a statute of limitations on credit card debt, typically three to six years from the date of last activity — though some states extend to ten years. After that window, the debt is “time-barred” — collectors lose the legal right to sue. But it still exists, still affects your credit until the reporting window closes, and making any payment can reset the clock in some states.

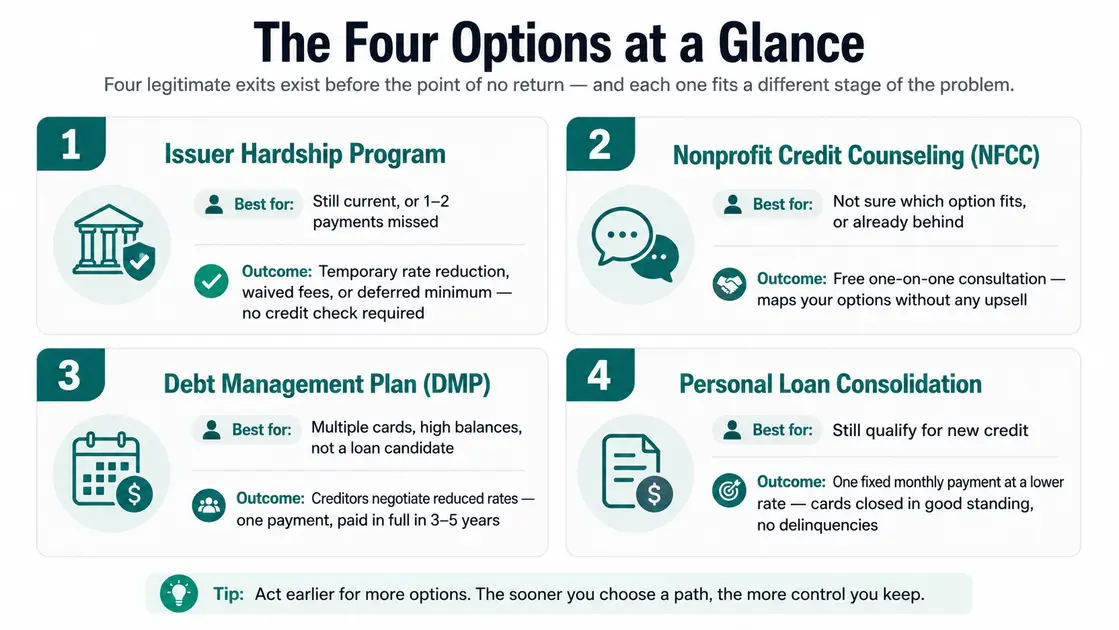

What Options Exist Before You Reach That Point?

The part that almost never surfaces in a Google search: most of these consequences are avoidable, and the options are accessible at stages most people assume are already too late.

Option 1 — Issuer Hardship Programs

Best for: Anyone who is still current on payments or has missed only one or two.

What you get: A temporary modification to your account terms — reduced interest rate, waived late fees, or a lower minimum payment for a set period (often three to twelve months).

Most major credit card issuers maintain formal hardship or forbearance programs. These programs were designed precisely because issuers would rather receive a modified payment than absorb a charge-off loss. You apply by calling your issuer directly and asking specifically for the hardship or financial assistance department. There’s generally no credit check, and it doesn’t automatically close your account. You just have to ask.

The key is timing. Calling before you miss a payment gives you the most leverage and the most options. Calling after you’ve already missed two or three doesn’t eliminate the option — but the terms may be less favorable. The CFPB’s credit card resources offer guidance on what to expect when making this call.

Option 2 — Nonprofit Credit Counseling (Free)

Best for: Anyone who isn’t sure which option fits their situation, or who has already missed payments and needs a full picture.

What you get: A free one-on-one consultation that covers your complete financial picture — income, debts, monthly expenses — and maps out your options without an upsell.

The National Foundation for Credit Counseling (NFCC) is the largest network in the U.S. Its member agencies are accredited, regulated, and legally required to provide free or very low-cost initial consultations. This one conversation often surfaces options people had no idea existed.

Option 3 — Debt Management Plans (DMPs)

Best for: People with multiple cards and high balances who need lower rates and a single structured payoff, but aren’t candidates for a personal loan.

What you get: The counseling agency negotiates directly with your creditors — often securing reduced interest rates, waived fees, and a single consolidated monthly payment. Accounts are paid in full within three to five years.

Through a DMP managed by an NFCC-member agency, you pay the agency; they distribute to creditors. A DMP does require closing the enrolled cards, which has a short-term effect on credit utilization — but that’s a far smaller long-term impact than a charge-off, settlement, or default.

Option 4 — Personal Loan Consolidation

Best for: People who still qualify for new credit and want to convert revolving card debt into a single fixed payment at a lower rate.

What you get: One fixed monthly payment, a rate typically lower than your current card APR, and cards that close as paid in full — no delinquencies, no settlement notation on your report.

Average credit card APRs have been running well above 20% — Federal Reserve G.19 data tracks this monthly. Personal loan rates for qualified borrowers often come in meaningfully lower, reducing both the monthly payment and total interest paid. The revolving pressure ends the day you close those balances. Checking your rate through a comparison tool like Buddy Loan uses a soft pull — it won’t affect your credit score.

Still Qualify for a Personal Loan? This Is How You End the Cycle.

Consolidating at a lower fixed rate stops the monthly interest bleed without any of the credit damage that comes from stopping payments. Checking available rates takes under two minutes and uses a soft pull — it won't affect your credit score.

Check Personal Loan Options →What Does “Stopping the Worry” Actually Look Like?

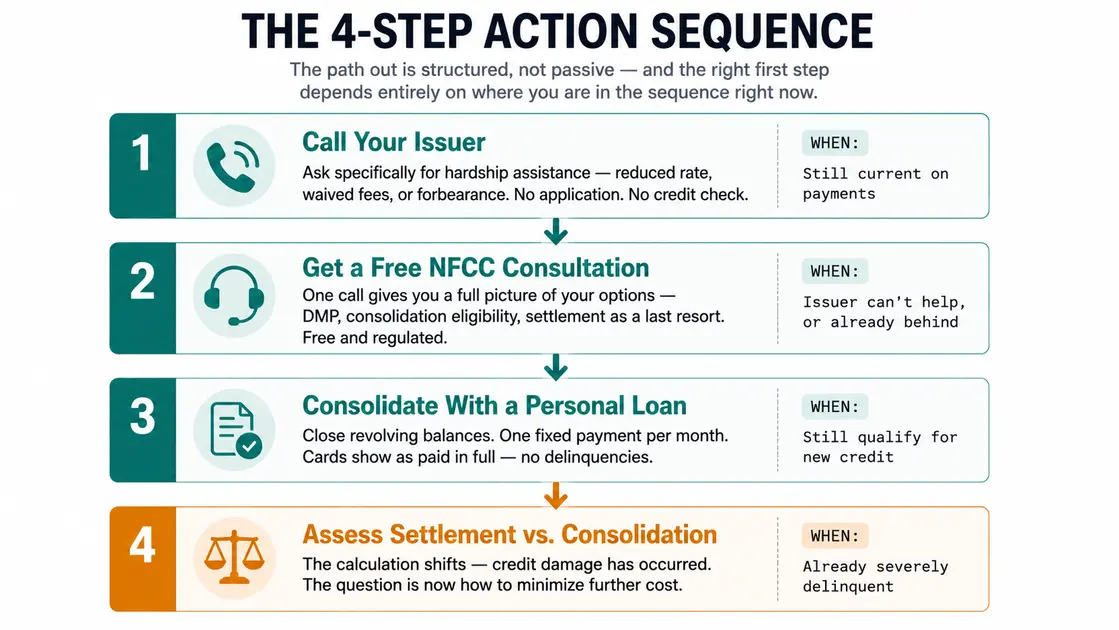

The search “stop paying credit card debt and stop worrying about it” isn’t a desire to defraud anyone — it’s a request for a way out that doesn’t require constant dread. That path exists, but it’s structured, not passive. Here’s what it looks like in practice.

Step 1: Call your issuer today and ask specifically for hardship assistance. Before you miss a payment, this is your lowest-friction option. Reduced rate, waived fees, temporary forbearance. It doesn’t require a new application or a credit check. The only thing required is the phone call. If the situation is broader — minimums barely manageable with no room to maneuver — getting out of debt when you’re broke covers the full six-step path, starting with what costs nothing.

Step 2: If the issuer can’t help or you’re already behind, get a free NFCC consultation. One call to an NFCC-member agency gives you a full picture of your options — DMPs, consolidation eligibility, whether settlement is even a realistic path. Free, regulated, and importantly: no upsell. These agencies make their money from small monthly program fees, not from steering you into products.

Step 3: If you still qualify for new credit, use a consolidation loan to restructure the debt. The revolving credit card pressure stops the day you close those balances. You make one fixed payment per month until the loan is paid off. The credit damage from the cards you pay off recovers over time — closed in good standing, no delinquencies.

Step 4: If you’re already severely delinquent, the decision shifts. Settlement versus consolidation is a different calculation at that point — one where some credit damage has already happened and the question is how to minimize further cost and resolve the situation. That comparison is covered in full in our guide to Debt Settlement vs. Consolidation.

Where Should You Go From Here If You’re Overwhelmed by Credit Card Debt?

Still current but struggling: Call your issuer’s hardship line before you miss a payment. Ask for a temporary rate reduction or payment deferral. Document the call — date, rep name, and exactly what was offered. That documentation protects you if the terms aren’t applied correctly.

Already behind: Get a free credit counseling session via the NFCC. If a Debt Management Plan fits your situation, they’ll set it up. If a consolidation loan is an option at your current credit standing, that comparison matters — covered in our guide to Debt Consolidation vs. Balance Transfer.

Severely delinquent or in collections: The decision tree changes significantly at this stage. Our guide to Debt Settlement vs. Consolidation covers the honest cost comparison between these two paths, including the credit damage and tax implications of settlement (the IRS treats forgiven debt as taxable income — lenders are required to issue a 1099-C for $600 or more, but the tax obligation applies to any cancelled amount; one exception: if you were insolvent at the time of settlement, you may qualify to exclude some or all of it).

Frequently Asked Questions

What actually happens if I just stop paying my credit card?

Within 30 days: a late fee of up to $30, a potential penalty APR of up to 29.99% applied to your existing balance, and a 30-day late mark on all three credit bureau reports. By 180 days, the account is charged off and sold to a debt collector. The debt doesn't disappear — it just moves to a collector with more aggressive tools. The CFPB explains the charge-off process in detail.

How long before a missed payment affects my credit score?

One missed payment is reportable once you're 30 days past due. According to myFICO, that single late mark can drop a FICO score by 60 to 110 points or more — the higher your starting score, the steeper the drop. A 90-day late causes more damage than a 30-day late, even if it's the same underlying missed payment — each tier is scored separately.

Will my credit card company actually work with me if I can't pay?

Yes, more often than people assume — especially before you've missed a payment. Major issuers maintain hardship programs specifically to reduce the risk of charge-offs. They can reduce your interest rate, waive fees, or defer minimums. Call before you miss the payment, and ask explicitly for the hardship or financial assistance department.

What is a credit card hardship program and how do I qualify?

A hardship program temporarily modifies your account terms — lower interest rate, waived fees, reduced minimum — in exchange for a commitment to keep paying. Common qualifying situations include job loss, medical hardship, or a documented income reduction. You apply by calling your issuer; there's no credit check and it doesn't automatically close your account. The CFPB's credit card resources offer guidance on what to expect.

Can a credit card company sue me for unpaid debt?

Yes. Once sold to a collector, that collector can sue for the balance plus interest. A judgment can lead to wage garnishment or a bank levy. That said, every state has a statute of limitations — typically three to six years from last activity, though some states allow up to ten years — after which the debt is time-barred and can't be litigated. It still exists and can still be reported; it just can't be sued on.

How long does a credit card charge-off stay on my credit report?

Seven years from the charge-off date, per the Fair Credit Reporting Act. Since charge-off happens ~180 days after the first missed payment, the item effectively drops off your report about 7.5 years from when you first went delinquent. Paying or settling updates the status — which helps — but doesn't remove the entry or reset the clock.

Is it better to settle credit card debt or consolidate it?

For most people who still qualify for a personal loan, consolidation wins — lower total cost, no settlement notation, and no cancelled-debt tax bill (the IRS treats forgiven settlement amounts as taxable income; consolidation pays the balance in full, so nothing is forgiven). Settlement is the more relevant option when credit damage has already occurred and new credit isn't accessible. The full comparison is covered in our guide to Debt Settlement vs. Consolidation.

Stop the Pressure Without the Credit Damage

If you still qualify for a personal loan, a lower fixed rate ends the monthly bleed — one payment, defined payoff date, no default on your record. Multiple lenders in one check, with no obligation and no hard pull to check your rate.

See What Rate You May Qualify For →Financial Decision Lab provides informational content only. This article is not financial advice. Readers should consult a licensed financial professional for guidance specific to their situation.