- The mathematically optimal debt payoff method — the avalanche — costs less in interest but fails more often in practice. Here's why, and how to identify which one you'll actually finish.

- The single factor that determines which method fits your situation — and it's not your total debt balance or your interest rates.

- What the real-world completion data shows about people who choose each method — and the one scenario where switching mid-plan is not only acceptable but recommended.

You have multiple debts. You’re already making payments. You’re already doing the right thing. But here’s the problem most people run into: when you’re juggling three, four, or five balances at once, spreading your payments thin means you’re making slow progress everywhere and fast progress nowhere.

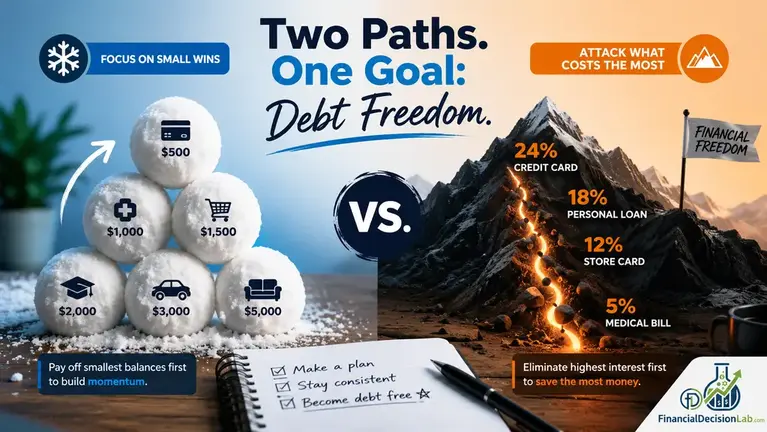

Both the debt snowball and the debt avalanche solve this the same way — stop spreading, start focusing. Pick one debt, throw everything extra at it, and when it’s gone, roll that freed-up payment into the next target. The mechanic is identical. The only difference is the order you pick your targets. And that single ordering decision determines how much interest you’ll pay, how long this takes, and — critically — whether you’ll actually stick with it.

Most people who’ve tried to pay down debt and stopped didn’t fail because they chose the wrong method. They stopped because the plan stopped feeling like it was working. That’s the thing this article is actually trying to solve.

Here’s how to pick the right one for you.

Which One Is Right for Your Situation?

The answer depends on two things: your psychology, and whether you’ve tried this before.

Answer three quick questions:

1. Do you have any debt with an APR above 20%? → Yes: Start with the Avalanche. The daily interest cost of waiting on a 22–26% APR balance is measurable and material. Math wins here.

2. Have you started a debt payoff plan before and abandoned it? → Yes: Start with the Snowball. The momentum from clearing a small balance early is worth more than the interest savings on paper.

3. Are all your balances and rates in a similar range? → Yes: Either method works. The difference in total interest paid will be minimal. Pick the one you’ll actually execute — then read Section 4 for a move that accelerates both.

Note: You can switch methods mid-way. More on that in the FAQ.

If you’re still not sure, the two questions that usually settle it: how many separate debts do you have, and have you tried to pay this down before? More than four debts and a previous failed attempt almost always points to snowball.

How Does Each Method Order Your Debts?

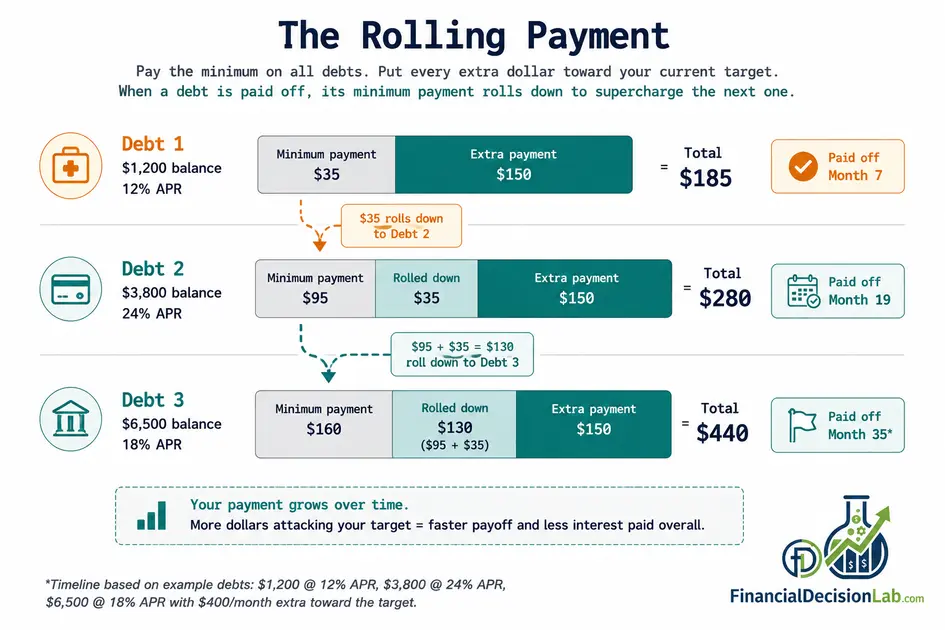

The core mechanic is the same for both. Every month, you pay the minimum on every debt except your current target. Every extra dollar you have goes at that one target. When it’s paid off, you take that account’s minimum payment and add it to your extra-payment budget — that’s the “snowball” or “avalanche” rolling forward. You repeat until there’s nothing left.

The difference is entirely in how you sort the list.

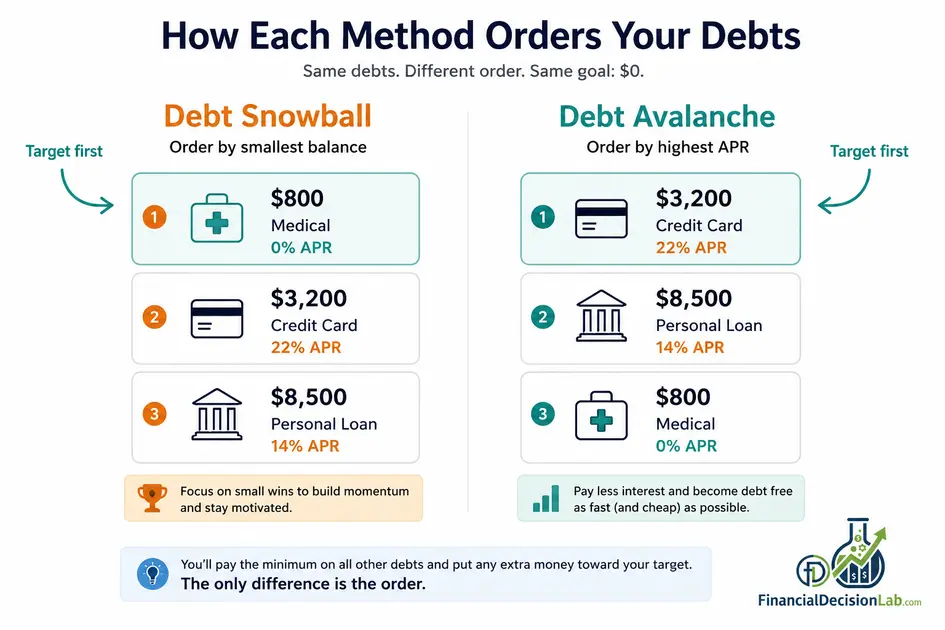

The Debt Snowball

Sort your debts smallest balance to largest. Interest rates don’t factor into the order at all. Your target is always the account with the least money owed, no matter what it’s costing you.

Here’s why this works in practice: clearing an account completely — watching a balance hit $0 — creates a concrete, measurable win. Research on debt repayment behavior consistently shows that eliminating individual accounts — not just reducing balances — is the strongest predictor of staying on a payoff plan long-term. You’re not just paying off debt; you’re building the habit of paying off debt. Each eliminated account resets your motivation for the next one.

Example: You have three debts — an $800 medical bill at 0% APR, a $3,200 credit card at 22% APR, and an $8,500 personal loan at 14% APR. The snowball starts with the $800 medical bill. It’s the fastest win available, and clearing it removes an account from your mental load entirely.

The Debt Avalanche

Sort your debts highest APR to lowest. Balances don’t drive the order. You’re targeting wherever the interest rate is most expensive, regardless of how much you owe.

Here’s why this wins mathematically: high-rate debt compounds daily. Credit cards calculate interest using a daily periodic rate (your APR ÷ 365), applied to your average daily balance — a mechanism the CFPB explains in detail. A 26% APR card isn’t just costing you more each month — it’s actively growing while you’re paying down everything else. Eliminating the most expensive rate first means you stop the most costly bleeding as quickly as possible.

Same example, avalanche version: You start with the $3,200 credit card at 22% APR, not the small medical bill. The first payoff takes longer to reach than under the snowball — you’re paying down a bigger balance — but you’ve eliminated the debt that was generating the most interest the entire time.

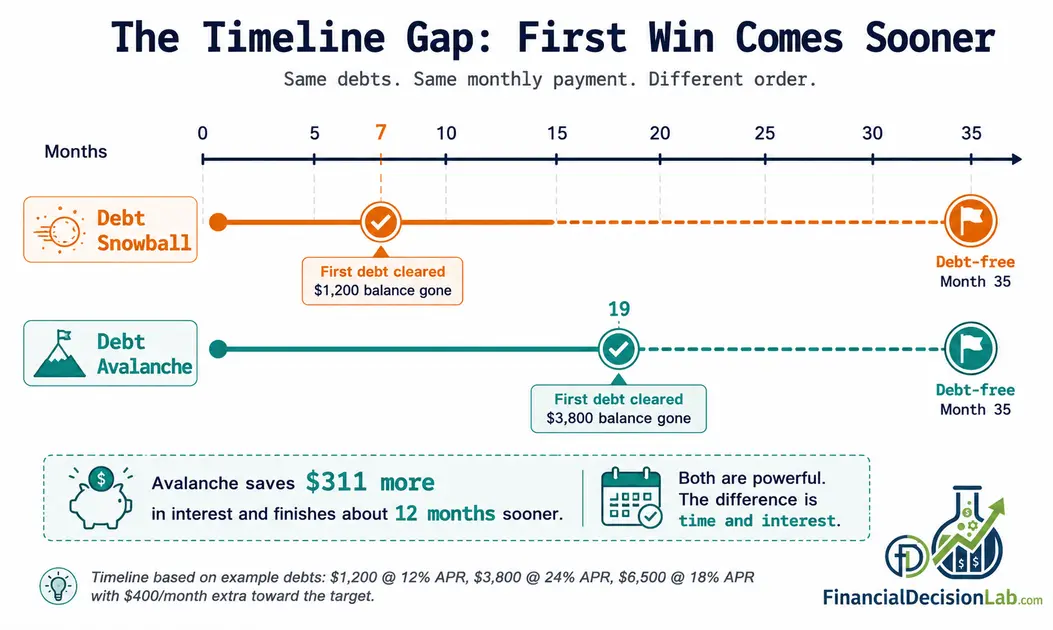

The math gap between the two methods varies depending on your specific debt mix. Here’s what it looks like on a stack where the two methods genuinely diverge — the highest-APR debt is not the smallest balance.

Which Method Saves More Money?

Let’s run the numbers on a realistic three-debt scenario where the methods produce different payoff orders. The APR figures used are within the current range tracked by the Federal Reserve’s consumer credit data:

- Debt A: $1,200 low-rate card, 12% APR, $35 minimum

- Debt B: $3,800 credit card, 24% APR, $95 minimum

- Debt C: $6,500 personal loan, 18% APR, $160 minimum

- Extra payment budget: $150/month above minimums

| Debt Snowball | Debt Avalanche | |

|---|---|---|

| Payoff order | A → B → C | B → C → A |

| Months to debt-free | ~35 months | ~35 months |

| Total interest paid | ~$3,655 | ~$3,344 |

| Interest saved vs. min-only | ~$4,145 | ~$4,456 |

| First debt cleared | Month 7 (Debt A — $1,200) | Month 19 (Debt B — $3,800) |

| Psychological difficulty | Lower | Higher |

| Best for | Motivation risk | Pure math optimization |

Look at the first debt cleared row. The snowball delivers a payoff win at month 7 — Debt A is gone, and its $35 minimum rolls forward into the next target. The avalanche doesn’t reach its first payoff until month 19, because Debt B ($3,800 at 24% APR) is a larger balance to eliminate, even though taking it out first stops the most expensive interest accumulation.

The avalanche saves about $311 more in this example over 35 months. The snowball clears its first account 12 months sooner. Both methods save roughly $4,100–$4,500 compared to paying minimums only — the choice between them is about the path, not whether to concentrate payments at all. The larger the high-rate balance relative to everything else, the more the avalanche pulls ahead in total interest saved.

Debt Payoff Calculator

Snowball vs. Avalanche — Your Numbers

Enter your debts and monthly extra payment. The calculator runs a month-by-month simulation for three strategies and shows exact payoff timelines, total interest, and savings versus minimum payments only.

Want to Lower the APR Before You Start?

A personal loan at a lower rate reduces the interest cost under either method. Check options without affecting your credit score.

See If You Qualify for a Lower RateHow Do You Actually Start Your Debt Payoff Plan This Week?

Knowing the theory isn’t the hard part. Starting is. Here’s a step-by-step plan you can execute this week, regardless of which method you’ve chosen.

Steps That Apply to Both Methods — Do These First

Step 1: List every debt in one place. Creditor name, current balance, APR, minimum monthly payment. Pull from your credit card portals, loan servicers, and your last statements. This takes about 20 minutes and most people have never done it as a single exercise. Seeing the full picture in one place changes your relationship to the problem.

Step 2: Identify your true minimum payments. This means the actual contractual minimum — not what you’ve been auto-paying, not a round number you chose. Your floor is the number below which you’ll be hit with late fees or delinquency marks.

Step 3: Find your real extra-payment number. After rent or mortgage, groceries, utilities, and every minimum payment, what’s left? Write that number down. Even $75 a month directed at one account changes the math materially. Don’t skip this step — it’s the budget reality check that makes the whole plan executable. If you use a percentage-based framework, this number lives inside the 20% savings and debt paydown bucket — and if that bucket is nearly empty because essential expenses are consuming more than half of take-home pay, that’s the root constraint. The 50/30/20 rule explains why that happens structurally. If you haven’t built that full picture yet, a seven-step monthly budget walks from take-home pay through each cost category to the exact surplus number this step requires.

One note before you allocate every extra dollar to debt: if you have no financial buffer at all, set aside your first $500 in a separate savings account before starting the payoff plan. Without it, one unexpected expense immediately reloads the balance you just paid down. Here’s how to build a starter emergency fund even while carrying debt.

Step 4: Choose your method. Use the decision block earlier in this article if you haven’t already. If you’re genuinely unsure, run both through the calculator. The goal is to pick one and commit — not to optimize indefinitely.

If You’re Using the Snowball

Step 5: Sort your debt list smallest balance to largest. The first row is your target this month.

Step 6: Every month, pay minimums on all other debts. Direct every extra dollar at the top row.

Step 7: When the top row hits zero, cancel the account if it’s a store card or a credit card you don’t need. Add its former minimum payment to your extra-payment budget. Move to the next row.

Step 8: Don’t adjust your extra payment budget when you get a raise or a bonus. Add those windfalls directly to the current target balance instead.

If You’re Using the Avalanche

Step 5: Sort your debt list highest APR to lowest. The first row is your target.

Step 6: Same mechanic — minimums everywhere else, all extra at the high-rate target.

Step 7: Track the interest charge on that top account every month. Watching the daily interest cost fall as the balance drops is the avalanche’s version of a psychological win. Use it.

Step 8: If motivation dips during a long payoff slog on a large high-rate balance, you have permission to redirect to the next-smallest balance for one full payoff cycle. Clear that quick win, then return to the avalanche order. The interest cost of that detour is usually small. The cost of quitting entirely is large.

The plan that runs for 18 months beats the optimal plan that stops after four.

If your situation has changed — new debt added, income drop, a balance transfer — re-sort your list before the next payment cycle. The method doesn’t change. The order does.

What If You Could Lower the APR and Speed Up Either Method?

A personal loan at a lower rate than your credit cards reduces total interest cost regardless of which payoff method you’re using — and it changes the math on both.

If you ran the calculator above and the total interest number made you wince, there’s a lever worth considering before you lock in your payoff order.

Both the snowball and the avalanche assume your interest rates are fixed. They aren’t.

A personal loan at 10–15% APR used to pay off a credit card charging 22–26% doesn’t change which method you’re using. It lowers the interest cost across the entire time you’re executing the plan. That’s a different lever entirely — and it works regardless of your method.

If you’re running the snowball: consolidating your highest-rate balance at a lower APR shrinks the math gap between snowball and avalanche. You get the psychological benefits of the snowball with less interest penalty for ignoring the rate order.

If you’re running the avalanche: a lower APR on your top target means you reach that first payoff month sooner. The rollover payment that kicks in when it’s gone is larger. Every subsequent step in the plan accelerates.

The question worth asking before you start either method is whether your current APRs are the best rates available to you — or just the rates you defaulted into. For a detailed look at how to use a personal loan to replace high-rate card debt, see using a personal loan to pay off credit card debt.

See if a personal loan rate beats your current credit card APR — compare options in under 2 minutes. → Check loan options

Frequently Asked Questions

Which method saves more money overall?

The avalanche always wins in pure interest saved — no exceptions. A higher-rate balance always costs more the longer you carry it, and the avalanche eliminates those costs first. That said, the snowball can produce a better total financial outcome if it prevents you from abandoning the plan. Studies on debt payoff behavior — including research published in the Journal of Marketing Research — show meaningful differences in completion rates between the two approaches, with snowball users more likely to stick with the plan long-term. The right question isn't "which method saves more interest?" — it's "which method will I actually finish?"

What if two debts have similar balances and similar interest rates?

If the balances and rates are within 10–15% of each other, the ordering decision makes almost no mathematical difference. Pick the one with the marginally higher APR if you want to be precise. One useful exception: if one of the debts has a fixed end date — say, a car loan with 18 months remaining — clearing it first frees the minimum payment sooner, even if the rate is slightly lower.

Can I switch from one method to the other mid-way?

Yes — with one condition. Don't switch mid-cycle on your current target debt. Finish the payoff you've already started, then re-sort your remaining list using the new method's ordering logic. Switching midstream on a target debt means you've paid down a balance without completing the win, which is the worst outcome of both methods.

What if I have a mix of very high-rate and very high-balance debt?

High-rate, high-balance debt is where the two methods diverge most sharply — and where ignoring rate order has a real dollar cost. A $12,000 credit card balance at 28% APR generates roughly $280 per month in interest at minimum payment. At that level, the interest cost of ignoring rate order is no longer a rounding error — it's a material drag on everything else you're doing. Run the calculator to see the exact monthly interest on your high-rate balance. That number alone usually makes the decision.

Is it worth including car loans and student loans in my payoff plan?

List them for a complete picture, but treat them differently from credit cards. Federal student loans carry income-driven repayment options and potential forgiveness programs that change the calculus. Car loans are fixed-term and often lower-rate. For most people, credit card and high-rate personal loan balances in the 18–28% APR range are the highest-yield targets by a significant margin. Focus extra payment dollars there first.

How do I start paying down debt when I can only afford minimums?

Minimum-only payments aren't a neutral holding pattern — on a high-rate card, they can keep you in repayment for a decade. On a 22% APR card, minimum payments on a $4,000 balance can stretch repayment to 15 years or more, with total interest approaching or exceeding the original balance itself. The CFPB's credit card repayment tools let you model the exact cost on your own balances. If there's genuinely no room for extra payments, the first step is finding it — a subscription audit, a temporary spending pause on a single category, or a one-time income source. Even $30 to $50 above minimums on one account changes the math materially. For a more complete path that starts before the payoff method choice — covering hardship programs, assistance programs, and creating margin first — see how to get out of debt when you're broke.

Does it matter which card I pay off first if I'm also doing a balance transfer?

Yes, and this interaction is often overlooked. A balance transferred to a 0% intro APR card temporarily exits the avalanche order — its effective rate is 0% during the promotional period. Your avalanche target becomes the next-highest rate on your remaining list. Re-sort your debt list after every transfer and again when the intro period expires. A 0% card reverting to a 24% regular APR needs to re-enter the avalanche at the top of your list. For a deeper look at when a balance transfer makes more sense than consolidation, see debt consolidation vs. balance transfer.

What if one of my debts is in collections?

A collections balance doesn't slot naturally into either method. There's often no "minimum payment" in the traditional sense, and the balance may be negotiable — sometimes significantly. Before folding a collections account into your payoff plan, verify the balance and its age, confirm the debt is yours, and check whether it's within your state's statute of limitations for collections. If it is, negotiate a settlement amount directly before or alongside your regular payoff plan. A collections account handled separately is not a failure of your method — it's a parallel process.

What Is the Move That Matters Most When Starting Debt Payoff?

Both methods work. Both save thousands over minimum-only payments. The difference between them — in the example above, $311 over 35 months — is real, but it’s not the number that determines whether you come out of debt in three years or stay in it for ten.

The number that determines that is whether you start this week and keep going.

Pick the method that matches how you’re wired — the one that’s going to feel like it’s working at month 4, not just month 1. Run your actual debts through the calculator above. Write the payoff order down somewhere you’ll see it. Then start.

The debt payoff method that gets completed beats the optimal method that gets abandoned — every time.